Dealing with an insurance claim denial can be frustrating. A rebuttal letter for insurance claim denial is your chance to fight back. It’s a formal way to challenge the insurance company’s decision. The goal is to convince them to reconsider and pay your claim.

This article is your guide to crafting a winning response. We understand writing these letters can be tough. That’s why we’ve got your back. We’ll provide rebuttal letter examples and samples. You can easily adapt these insurance claim denial rebuttal letter templates to your specific situation.

Think of it as having a cheat sheet. We aim to simplify the process. Use our templates to strengthen your case. Successfully writing a rebuttal letter can feel empowering. Get ready to advocate for yourself and overturn that denial!

[Your Name/Your Company Name]

[Your Address]

[Your City, State, Zip Code]

[Your Email Address]

[Your Phone Number]

[Date]

[Insurance Company Name]

[Insurance Company Address]

[Insurance Company City, State, Zip Code]

Subject: Rebuttal of Claim Denial – [Claim Number: Your Claim Number]

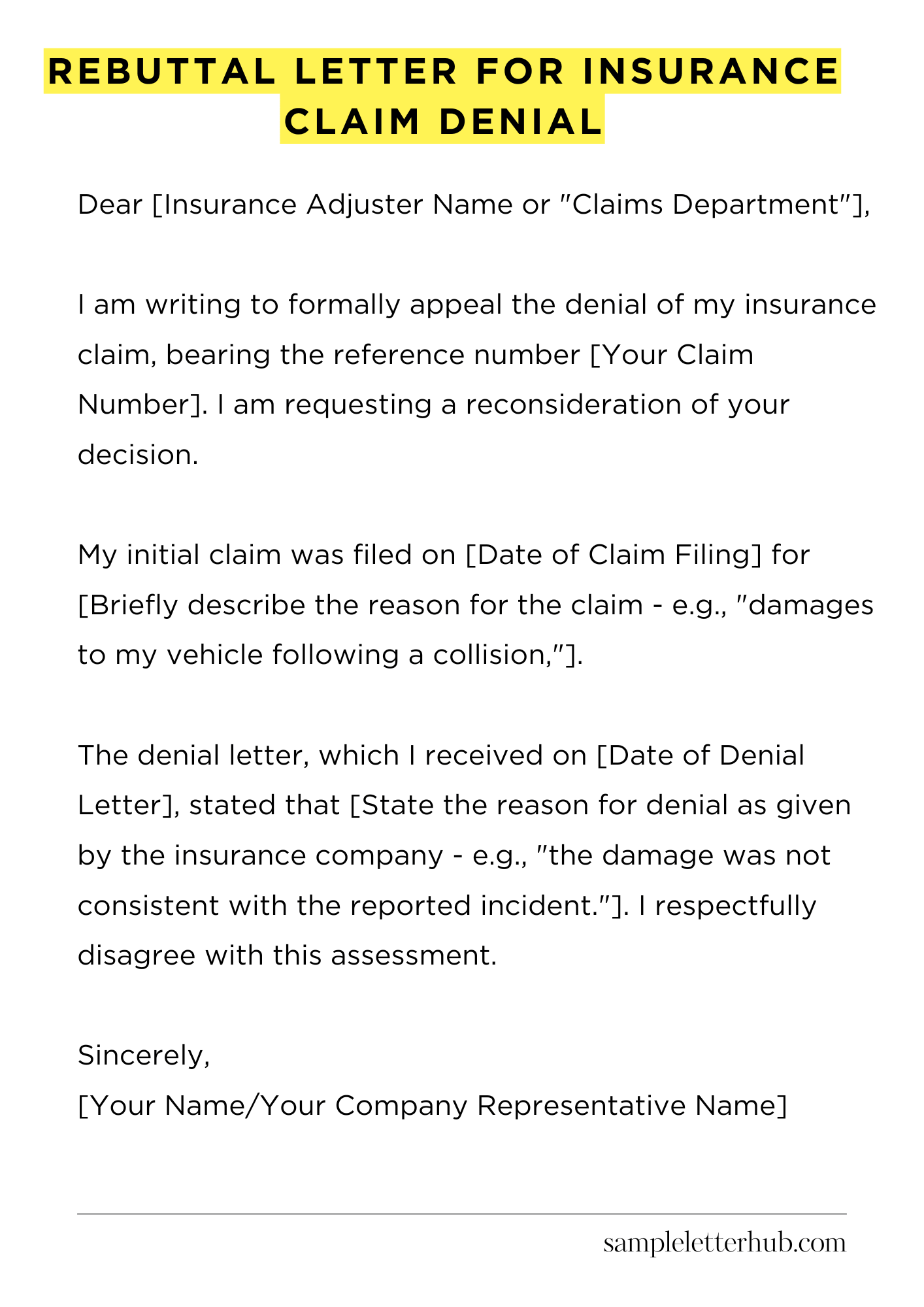

Dear [Insurance Adjuster Name or “Claims Department”],

I am writing to formally appeal the denial of my insurance claim, bearing the reference number [Your Claim Number]. I am requesting a reconsideration of your decision.

My initial claim was filed on [Date of Claim Filing] for [Briefly describe the reason for the claim – e.g., “damages to my vehicle following a collision,”].

The denial letter, which I received on [Date of Denial Letter], stated that [State the reason for denial as given by the insurance company – e.g., “the damage was not consistent with the reported incident.”]. I respectfully disagree with this assessment.

I believe the denial is based on an inaccurate understanding of the events. Allow me to clarify the situation further. The incident, as I reported, involved [Provide a clear and concise account of what happened. Include specific details.

This could be a couple of sentences or a small paragraph]. Following this, the damage observed on the vehicle was consistent with the described event.

To support my claim, I have included [List any supporting documents you are including – e.g., “photographs of the damage,” “police report,” “witness statements,” “repair estimates.”]. These documents provide additional evidence to substantiate my version of events and the resulting damages. They should help clear any doubts.

I kindly request that you review these materials thoroughly. I am confident that upon careful consideration, you will find sufficient grounds to overturn the denial. It is important to me, so please give it a good look.

I am available to provide any further information or clarification you may require. Please feel free to contact me at your earliest convenience. I am happy to help in any way I can to get this resolved.

Thank you for your time and attention to this matter. I look forward to your positive response and a favorable resolution.

Sincerely,

[Your Name/Your Company Representative Name]

How to Write Rebuttal Letter for Insurance Claim Denial

Receiving an insurance claim denial can be a frustrating experience. But don’t despair! A well-crafted rebuttal letter can often overturn the initial decision. Your aim is to persuasively present a compelling case, supported by evidence, to convince the insurance provider to reconsider. This guide will help you construct a potent response.

1. Understanding the Denial: Deconstructing the Rationale

Before you begin, scrutinize the denial letter thoroughly. Carefully dissect the insurer’s explanation for rejecting your claim. Identify the specific reasons cited.

Pinpoint the clauses, exclusions, or policy interpretations underpinning the denial. Take meticulous notes; this is your starting point. Knowing the precise grounds for denial is paramount to formulating a targeted rebuttal.

2. Gathering Your Ammunition: Assembling the Supporting Data

Your rebuttal letter is only as strong as the evidence you provide. Compile all pertinent documentation. This may include the original insurance policy, medical records, invoices, photographs, witness statements, and any other evidence that supports your claim.

Scrutinize your policy and ensure your documentation aligns with its verbiage. Authenticity and accuracy are paramount; remember to retain copies of everything for your records.

3. Crafting the Compelling Narrative: Structuring Your Rebuttal

Your letter should be structured logically and professionally. Begin with a polite yet firm salutation, clearly stating the policy number and claim number. In the opening paragraph, succinctly restate the claim and its denial.

The main body of your letter is where you systematically address each reason for denial. Refute each point with factual evidence and persuasive arguments, drawing upon your assembled documentation. Conclude with a clear and concise demand for reconsideration, reiterating your desired outcome.

4. Addressing the Preclusions: Navigating Policy Exclusions

Insurance policies are riddled with exclusions. If the denial hinges on a specific exclusion, address it directly. Explain why the exclusion does not apply to your case.

This may involve providing further context, highlighting the factual discrepancies, or arguing for a more favorable interpretation of the policy language. Consider consulting with an attorney if navigating complex exclusions.

5. The Art of Persuasion: Employing Persuasive Language

The tone of your letter should be professional and assertive, not accusatory or aggressive. Use clear, concise language. Avoid ambiguity. Support your claims with concrete evidence.

If appropriate, cite relevant legal precedents or expert opinions. Employ persuasive techniques such as emphasizing the benefits of resolving the claim, showcasing potential reputational risks for the insurer, and painting a clear picture of the situation. Remember, the goal is to convince the claims handler to change their mind.

6. Presenting Your Case: Formatting and Presentation

The visual appeal of your letter matters. Ensure a professional format. Use a standard font (e.g., Times New Roman or Arial) and a readable font size. Proofread meticulously for any grammatical errors or typographical mistakes. Include all pertinent contact information and date your letter appropriately.

Consider sending your rebuttal via certified mail with a return receipt requested to confirm delivery and establish a documented record. Keep a copy of your letter and all supporting documentation.

7. Seeking Augmentation: Legal Counsel and Additional Support

If your claim involves significant sums or complex policy language, consider consulting with an insurance attorney. An attorney can review your case, provide legal advice, and assist in preparing your rebuttal letter.

They can also represent you in negotiations with the insurance company. Even if you handle the initial rebuttal yourself, consulting with an attorney can provide valuable insights and ensure your rights are protected. Other resources, such as consumer advocacy groups, may also offer guidance and support.

FAQs about Rebuttal Letter for Insurance Claim Denial

What is a rebuttal letter for an insurance claim denial, and why is it important?

A rebuttal letter is a formal document you submit to your insurance provider to dispute their decision to deny your claim. It’s a crucial step because it gives you a chance to present additional information, challenge the reasons for denial, and potentially have the decision reversed. Without a well-crafted rebuttal, you may lose your right to benefits for the denied claim.

What information should I include in a rebuttal letter?

Your rebuttal letter should include the following key information: Your policy information (policy number, etc.), a clear statement of disagreement with the denial, a detailed explanation of why you believe the denial is incorrect, any supporting evidence (medical records, photos, witness statements, etc.)

What are the common reasons for insurance claim denials, and how do I address them in a rebuttal?

Common denial reasons include lack of medical necessity, pre-existing conditions, policy exclusions, incomplete documentation, and incorrect coding. In your rebuttal, directly counter each denial reason with evidence and explanations.

For example, if the denial cites lack of medical necessity, provide medical records and doctor’s notes that demonstrate the treatment was medically appropriate. If it’s a documentation issue, resubmit all necessary documents.

What is the timeframe for submitting a rebuttal letter, and what happens if I miss the deadline?

The timeframe for submitting a rebuttal letter is usually specified in your insurance company’s denial letter. It’s crucial to adhere to this deadline; otherwise, you may forfeit your right to appeal the denial.

The denial letter typically states the number of days you have to file a rebuttal letter. If you miss the deadline, the insurance company is under no obligation to review your case and your claim may be closed or denied. You can re-file but it might require more effort and time.

How can I increase my chances of a successful rebuttal?

To improve your chances of success, gather as much supporting documentation as possible, including medical records, expert opinions, and any other evidence that supports your claim.

Write a clear, concise, and well-organized letter that directly addresses the denial reasons. Consider consulting with a healthcare professional or an insurance claims expert to review your letter and provide additional guidance.

Additionally, keep copies of all correspondence and documents for your records. Remember, the letter is a formal document and needs to be professional.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study