Dealing with a life insurance claim denial can be incredibly stressful. A “Letter to Contest Denied Life Insurance Claim” is a formal way to dispute the insurance company’s decision. Its main purpose is to challenge the denial. This letter presents your case for payment. It provides further information or evidence. The goal is to convince the insurer to reconsider its decision.

Sometimes writing these letters can feel daunting. That’s where we come in. We will provide you with several sample “Letter to Contest Denied Life Insurance Claim” templates. These samples will help you. They will guide you in crafting your own persuasive letter. We aim to simplify the process.

This article is your guide to writing an effective contest letter. We’ll offer different examples. Each sample is tailored to specific denial reasons. Use these templates as a starting point. Adapt them to fit your individual circumstances and make the writing process much easier.

[Your Name/Law Firm Letterhead]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

RE: Claim Denial – Policy Number [Policy Number] – [Insured’s Name]

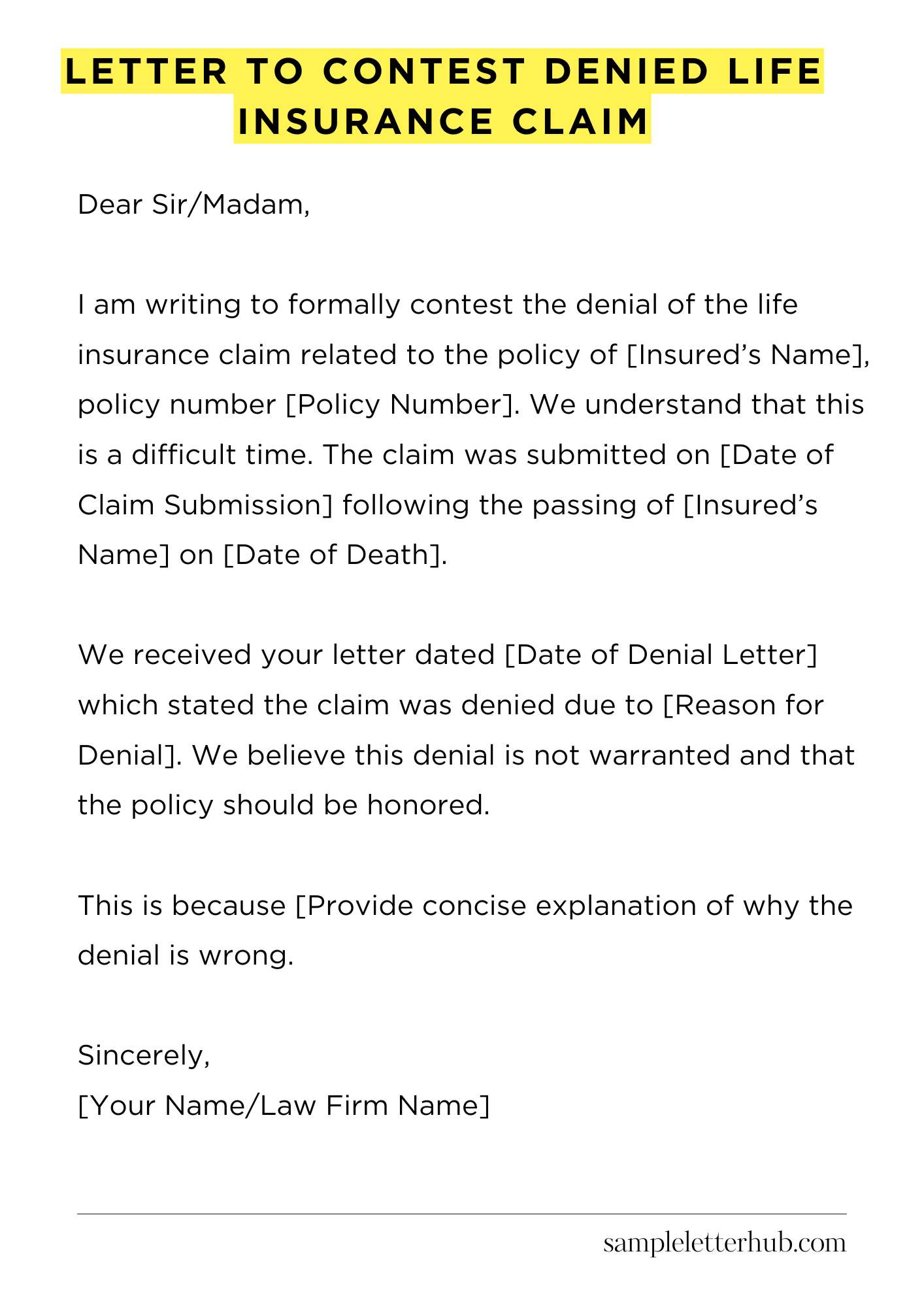

Dear Sir/Madam,

I am writing to formally contest the denial of the life insurance claim related to the policy of [Insured’s Name], policy number [Policy Number]. We understand that this is a difficult time. The claim was submitted on [Date of Claim Submission] following the passing of [Insured’s Name] on [Date of Death].

We received your letter dated [Date of Denial Letter] which stated the claim was denied due to [Reason for Denial]. We believe this denial is not warranted and that the policy should be honored.

This is because [Provide concise explanation of why the denial is wrong. For example: “the information provided about the insured’s health history on the application was correct” or “the death was not related to any pre-existing conditions”].

We have gathered information that supports our position. It clearly contradicts the reasons cited for denying the claim. Specifically, we have [Briefly list supporting documents or actions, e.g., “obtained the medical records from the insured’s primary care physician,” or “attached a sworn statement from a witness to the events leading to the insured’s death”].

Attached to this letter are copies of [List of attachments – e.g., medical records, witness statements, etc.]. We urge you to review these documents carefully.

The documents clearly demonstrate [Reiterate the key point, e.g., “that the death was not a result of a condition known to the insurance company”]. This information clearly contradicts the company’s decision.

We request that you reconsider your denial of the claim. We believe it is crucial to honor the terms of the policy. The beneficiaries are relying on these funds.

We look forward to your prompt response. Please contact me within [Number] days to discuss this matter further. We are available to answer any questions you may have.

Sincerely,

[Your Name/Law Firm Name]

How to Write Letter to Contest Denied Life Insurance Claim

Receiving a life insurance claim denial can be a devastating blow. It’s especially disheartening when you believe the beneficiary is rightfully owed the funds.

However, denial isn’t necessarily the final pronouncement. You have the right to contest the decision. Formulating a compelling letter of contestation is crucial. Here’s a stepwise guide to composing an effective appeal.

1. Initiate with Formality

Begin your letter with a formal salutation. Address the letter to the appropriate department within the insurance company – usually, it’s the Claims Department or the Appeals Department.

State the policyholder’s full name, policy number, and the date of the claim denial. Always reference the official denial notice details. Clarity and precision are paramount at this initial stage.

2. Articulate the Rationale for Contest

This is where you clearly outline the reasons why you’re contesting the denial. This section requires precision. Examine the denial notice closely. It will specify the grounds for the denial.

Dissect each reason. Then, construct counter-arguments. Provide comprehensive facts, data, or documents to invalidate the insurer’s rationale. Address each point directly. Demonstrate the factual inaccuracies within the denial. Your goal is to illuminate the flawed reasoning that led to the rejection.

3. Furnish Supporting Documentation

Evidence is the bedrock of a successful appeal. Assemble all the documentation that buttresses your case. This may include the original life insurance policy, medical records, death certificates, and any other pertinent documents that support the claim. The more comprehensive your supporting documentation, the stronger your position will be.

This will assist the insurance company to re-evaluate the claim objectively. Make high-quality copies. Send them certified mail with return receipt requested. This ensures a record of delivery.

4. Address Any Ambiguities

If there are any ambiguities or unclear statements within the denial notice, address them explicitly. Question any confusing language. Seek clarification. This can reveal the underlying inconsistencies in their conclusions. Your tenacity is a strength. Don’t hesitate to probe the insurer’s reasoning.

5. Highlight Policy Compliance

Affirm the policyholder’s adherence to all policy stipulations. If the denial alleges a breach of contract, demonstrate that the policyholder fulfilled every obligation.

If applicable, showcase that premiums were paid punctually. Show the meticulous adherence to every term outlined within the policy. This can strengthen your claim. It shows the legitimacy of the claim.

6. Showcase the Consequences of Denial

This section is where you highlight the impact of the denial on the beneficiary. Explain the financial hardship or emotional distress the denial has caused. While the focus should remain on the factual merits of the claim, acknowledging the human element can be poignant. It brings a personal touch to the case. This can often influence the decision-making process.

7. Demand Action and Finalization

Conclude your letter with a clear demand for reconsideration. State that you believe the claim should be approved. Specify a reasonable timeframe for the insurance company to review your appeal and render a decision. Include your contact information. Express your willingness to collaborate further if needed.

Always close with a professional and assertive closing, such as “Sincerely” or “Respectfully.” This reinforces your professionalism.

FAQs about Letter to Contest Denied Life Insurance Claim

What is a “Letter to Contest a Denied Life Insurance Claim” and why is it necessary?

A “Letter to Contest a Denied Life Insurance Claim” is a formal communication sent by a beneficiary or their legal representative to an insurance company when a life insurance claim has been denied.

It serves to dispute the denial, presenting arguments, evidence, and legal grounds to overturn the decision. It is necessary because it is often the primary mechanism to formally challenge the denial and initiate a review process, or prepare for litigation.

What information should be included in a letter contesting a denied life insurance claim?

A comprehensive contesting letter should include the policyholder’s and beneficiary’s identifying information, the policy details, the reasons provided by the insurance company for the denial, and a detailed counter-argument.

This counter-argument should address each reason for denial, supported by evidence such as medical records, policy language, witness statements, and any other relevant documentation. It must clearly state why the denial is incorrect.

What are the common reasons for denial of a life insurance claim, and how can they be addressed in a contest letter?

Common reasons for denial include misrepresentation on the application, failure to disclose pre-existing medical conditions, suicide exclusions, and issues related to the contestability period.

Addressing these in a letter requires a thorough examination of the policy and the denial reasons. For misrepresentation, provide evidence that the information was accurate or not material.

For non-disclosure, argue that the condition was not relevant or unknown. For suicide, dispute based on the policy terms and applicable laws. For contestability period issues, clarify and correct any misinformation. Present evidence which contradicts the insurer’s reasons.

What is the process after submitting a letter contesting a denied life insurance claim?

After submitting the letter, the insurance company typically reviews the information and may request additional documentation. This review may lead to the reversal of the denial, a settlement negotiation, or a continued denial.

If the denial is upheld, the beneficiary may have the option to escalate the matter through the company’s internal appeals process, file a complaint with the state’s insurance department, or pursue legal action by filing a lawsuit against the insurance company.

When should legal counsel be sought regarding a denied life insurance claim?

Legal counsel should be sought as soon as a claim is denied, especially if the denial appears unjustified, involves complex legal issues, or involves a substantial sum of money.

A lawyer can review the policy, assess the merits of the denial, draft a strong contest letter, negotiate with the insurance company, and represent the beneficiary in any subsequent legal proceedings. They can provide advice on state laws and guide the beneficiary through the appeals process and/or litigation, ensuring their rights are protected.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study