Ever received a letter from your insurance company canceling your policy *after* they’ve settled a claim? That’s what an insurance cancellation letter after claim settlement is all about. Insurance companies issue these letters for various reasons. The primary purpose is to officially notify you that your insurance coverage is ending. They are telling you they’re no longer offering you their insurance protection after a claim.

Dealing with insurance can be tricky. Writing letters, especially official ones, can feel overwhelming. We’re here to help! We’ve gathered helpful insurance cancellation letter after claim settlement samples. You’ll find templates, examples, and samples.

This article provides ready-made letter examples. They are easy to adapt. You can use these sample insurance cancellation letters to craft your own. Make the process smoother with our resources.

[Your Name/Company Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

Subject: Cancellation of Insurance Policy Following Claim Settlement

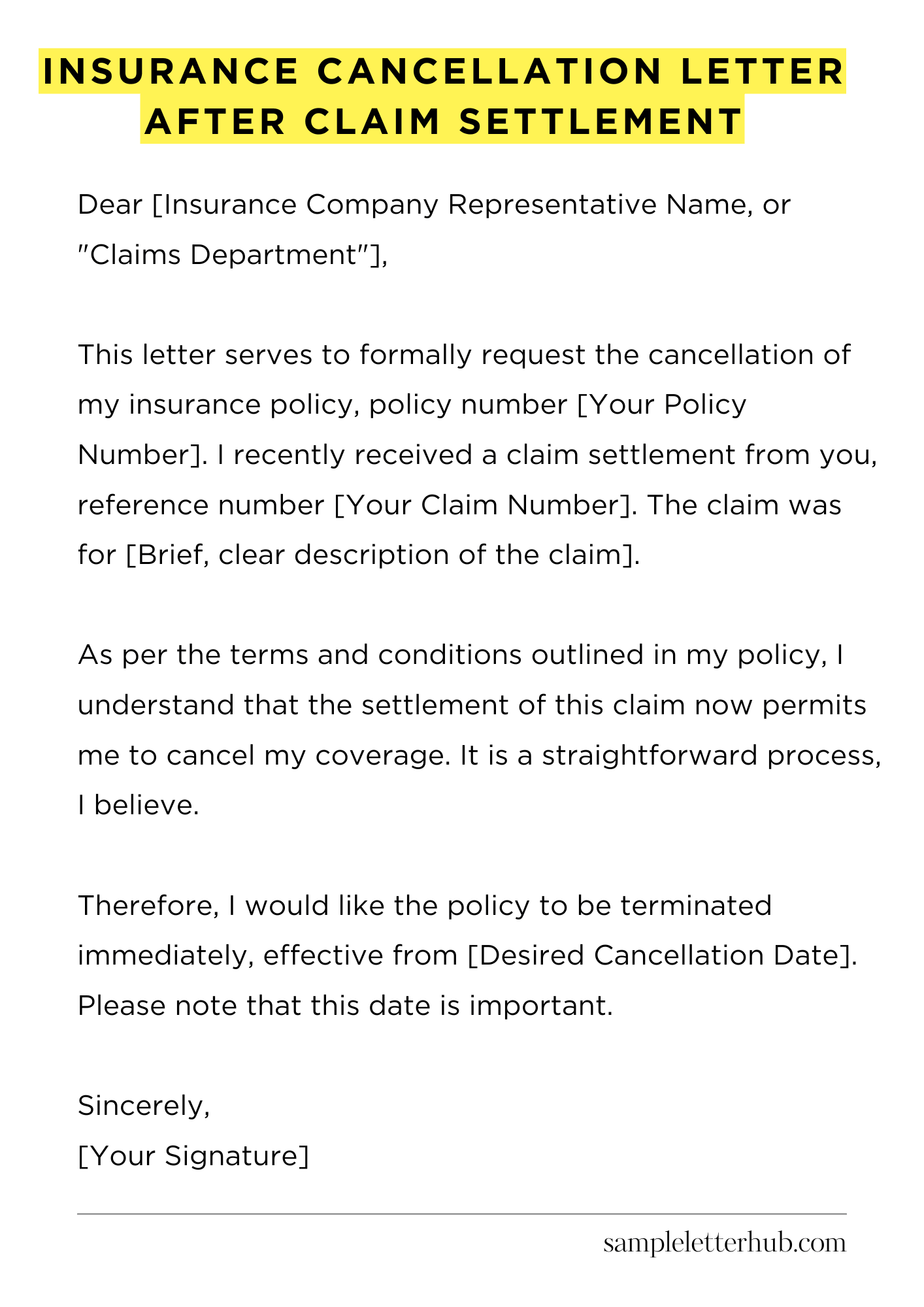

Dear [Insurance Company Representative Name, or “Claims Department”],

This letter serves to formally request the cancellation of my insurance policy, policy number [Your Policy Number]. I recently received a claim settlement from you, reference number [Your Claim Number]. The claim was for [Brief, clear description of the claim].

As per the terms and conditions outlined in my policy, I understand that the settlement of this claim now permits me to cancel my coverage. It is a straightforward process, I believe.

Therefore, I would like the policy to be terminated immediately, effective from [Desired Cancellation Date]. Please note that this date is important.

I kindly request that you confirm the cancellation in writing. Please also provide details regarding any potential refund of premiums, if applicable. This is important to know. I would appreciate it if the refund, if any, could be sent to [Your preferred method of payment: e.g., mailing address, bank account details].

Thank you for your time and assistance in this matter. I appreciate your prompt attention to this request. Your swift action will be greatly appreciated.

Sincerely,

[Your Signature]

How to Write Insurance Cancellation Letter After Claim Settlement

Congratulations, your insurance claim has been settled! You’ve navigated the often-treacherous waters of insurance bureaucracy, and now it’s time to finalize things. One crucial step remains: formally canceling your policy. This is where an insurance cancellation letter comes into play. It’s not just a formality; it’s a vital piece of documentation.

1. Initiate: The Genesis of Your Letter

Before you even think about penning your cancellation letter, you need to initiate the process. Review your policy documents. Pinpoint your insurance provider’s name, the policy number, and any specific cancellation protocols outlined within the contract. Familiarize yourself with the stipulated clauses for termination.

This preliminary assessment will be the foundational cornerstone of your letter. It’s the intellectual bedrock, so to speak.

2. The Salutation: A Formal Greeting

Begin your letter with a formal salutation. Address it to the appropriate department or individual at the insurance company. If you’re unsure, “To Whom It May Concern” is a safe, albeit generic, option. Be as specific as possible. This establishes a professional tone from the get-go. Precision in this section sets the stage.

3. Declare Your Intent: State Your Purpose Clearly

The core of your letter should clearly and unequivocally state your intent: to cancel your insurance policy. Include the policy number and the date you wish the cancellation to be effective. This date is critical. Ensure it aligns with your settlement agreement’s terms. This will protect your interest. Make sure there is no doubt in the readers’ mind.

4. The Claim’s Denouement: A Brief Acknowledgment

Briefly mention that your claim has been settled. This provides context for the cancellation request. Reference the claim number if possible. This reinforces the connection and provides a clear audit trail. It’s a succinct acknowledgement, a polite nod to the resolution.

5. Financial Tidbits: Addressing Premiums and Refunds

Inquire about any potential premium refunds. If you’ve overpaid, the insurance company has a duty to provide. Specify your preferred method of refund—check, direct deposit, etc. Include your bank details for clarity. Proactive handling of these financial elements will expedite the process and avoid future conflict.

6. The Formal Closure: Politeness and Professionalism

Conclude with a formal closing, such as “Sincerely” or “Respectfully.” Sign your name, and print your name clearly below your signature. If possible, provide your contact information (phone number and email address) for follow-up communication. This ensures clear communication. Make it easily accessible.

7. Delivery and Documentation: The Final Phase

Send your letter via certified mail with return receipt requested. This provides proof of delivery and confirmation of receipt. Keep a copy of the letter and the return receipt for your records.

Consider sending a duplicate copy via email for faster communication. This ensures every piece of documentation is accessible, for you. This meticulous approach provides a robust defense and safeguards your position.

FAQs about Insurance Cancellation Letter After Claim Settlement

What is an insurance cancellation letter after a claim settlement?

An insurance cancellation letter after a claim settlement is a formal notice issued by an insurance company informing a policyholder that their insurance coverage is being terminated following the resolution of an insurance claim.

This action can be taken for various reasons, most commonly due to an assessment of increased risk associated with the policyholder based on the filed claim, changes in risk profile, or policy violations.

Why would an insurance company cancel my policy after settling a claim?

Insurance companies might cancel a policy after a claim settlement for several reasons. One primary reason is that the claim could indicate an increased risk for the insurer.

Other factors can include policy violations, such as misrepresentation of information during the application process or a pattern of filing multiple claims. Furthermore, depending on the terms outlined in the policy, a significant claim payout may alter the company’s assessment of the risk they are willing to take on for a given policyholder.

Can the insurance company cancel my policy immediately after settling the claim?

The timeframe for cancellation after a claim settlement is usually governed by the terms of the policy and relevant state laws. The policy will specify the notice period that the insurance company must provide before the cancellation takes effect.

Generally, an insurance company must provide written notice to the policyholder, which can vary from a few days to several weeks. Immediate cancellation is uncommon unless there are egregious circumstances such as fraud.

What are my rights if I receive an insurance cancellation letter?

If you receive a cancellation letter, you generally have rights that are usually defined by your policy and the laws of your state. These may include a right to receive a written explanation for the cancellation, the opportunity to contest the cancellation, and the right to seek alternative insurance coverage.

It’s crucial to carefully review the cancellation letter for specific information on appeal procedures and timeframes. You might also have the option to file a complaint with your state’s insurance regulatory agency, especially if you believe the cancellation is unwarranted or discriminatory.

How can I find new insurance coverage after my policy is canceled?

Finding new insurance coverage after a cancellation can be challenging, but it’s essential. Begin by contacting several insurance companies and insurance brokers to compare rates and policies. You may need to provide details about your cancellation and the underlying claim history.

The cost of insurance may be higher due to the cancellation, and certain companies might refuse coverage. You may need to explore options like the state’s assigned risk pool (also known as the Fair Access to Insurance Requirements or FAIR Plan), which provides coverage for those unable to obtain insurance through standard markets.

Consider speaking with an independent insurance agent, as they can search through multiple insurance providers to find the best available coverage for your situation.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study