Ever found your home violated? A break-in is a homeowner’s worst nightmare. After the shock, comes the claim. You’ll need to explain the incident to your homeowners insurance company. This explanation letter for break in homeowners insurance is crucial. It details what happened, what was taken, and the damage. This letter ensures a smooth insurance claim process.

Crafting this letter can feel overwhelming. Don’t worry, we’re here to help. We’ve got you covered with various explanation letter for break in homeowners insurance templates. They will also provide several samples of explanation letter for break in homeowners insurance. These ready-made examples will guide you. Writing your own is now a breeze.

Whether it’s your first time or you need a refresher, we have something for you. Our goal is to make things easier. These explanation letter examples will get you started quickly. Just customize the provided samples to fit your specific situation.

[Your Name/Insurance Company Letterhead]

[Date]

[Recipient Name]

[Recipient Address]

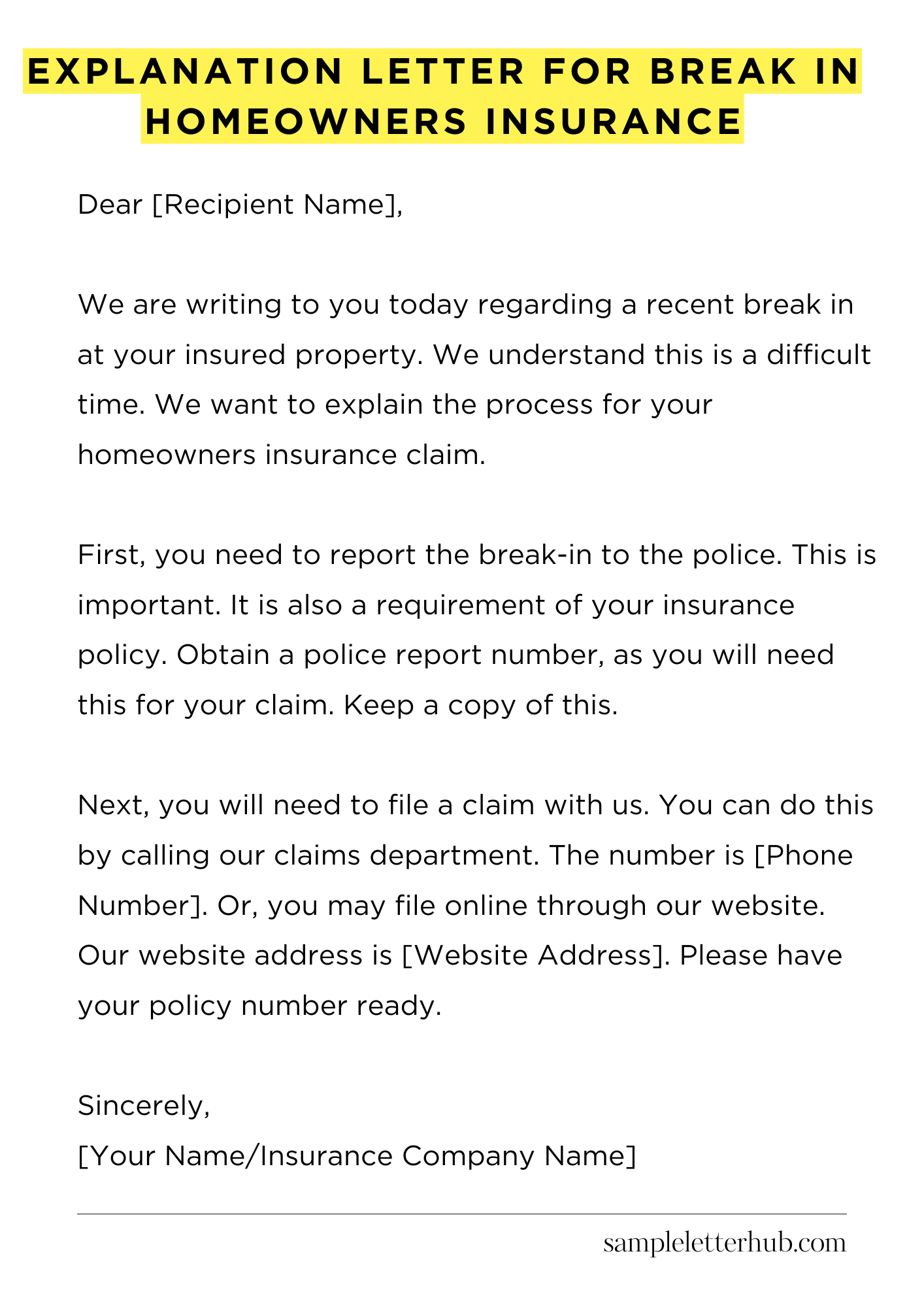

Dear [Recipient Name],

We are writing to you today regarding a recent break in at your insured property. We understand this is a difficult time. We want to explain the process for your homeowners insurance claim.

First, you need to report the break-in to the police. This is important. It is also a requirement of your insurance policy. Obtain a police report number, as you will need this for your claim. Keep a copy of this.

Next, you will need to file a claim with us. You can do this by calling our claims department. The number is [Phone Number]. Or, you may file online through our website. Our website address is [Website Address]. Please have your policy number ready.

When you file your claim, be prepared to provide details about the break-in. We need to know what was stolen or damaged. Describe how the break-in happened. The more information you can give us, the better. Photos and videos of the damage will be helpful.

An adjuster will be assigned to your case. The adjuster will contact you to discuss your claim. They may schedule a time to inspect the property. They will assess the damage. They will also determine the value of any lost or damaged items.

Your policy covers certain damages and losses. It is important to know your policy details. Your policy outlines the specific coverages and exclusions. We can help you understand your coverage.

We will work quickly to process your claim. Our goal is to make this process as smooth as possible for you. We understand the stress of a break-in.

We are here to help you get your life back to normal. Please do not hesitate to contact us if you have any questions. We are available to help.

Sincerely,

[Your Name/Insurance Company Name]

How to Write an Explanation Letter for Break in Homeowners Insurance

1. Grasping the Preliminaries: What is Required?

Before you even think about penning a single sentence, comprehend the foundational elements. You are crafting a formal missive, essentially a **supplication** for your insurer’s attention, explaining a break-in incident.

They require a concise, yet detailed account. Your goal is simple: to inform and elicit action – specifically, the processing of your claim. Carefully review your policy; understand what documentation the insurer mandates.

2. The Art of the Salutation: Addressing the Recipient Correctly

Begin with a professional greeting. This initial point sets the tone. Instead of a generic “To Whom It May Concern,” endeavor to identify the specific claims adjuster assigned to your case.

If you do not have their name, then find the correct contact person to send the letter. Then, use “Dear Mr./Ms. [Last Name]”. If unknown, use “Dear Claims Adjuster”. This displays due diligence.

3. Crafting the Core Narrative: Detailing the Incursion

This is the locus of your letter, the meat of the matter. Provide a chronological, unambiguous account of the break-in. Begin with the precise date and time of the occurrence.

Elaborate on how you discovered the intrusion and what observations you made, be meticulous. Include details such as points of entry (broken windows, forced doors), and the specific items stolen or damaged. Avoid hyperbole; maintain factual accuracy. Remember, the more detailed the information the smoother the claim becomes.

4. The Evidentiary Arsenal: Assembling Supporting Documentation

Include all the pertinent documentation that supports your claim. This is essential to its validity. Attach copies, not originals, of your police report (very important), a detailed inventory of stolen/damaged property, and receipts or proof of ownership where possible.

Provide any photographic evidence: images of the damage, and any existing images of the stolen items. This provides irrefutable substantiation.

5. Deciphering the Quantum of Loss: Calculating the Damages

This section involves a meticulous listing. Itemize each stolen or damaged item. For each item, specify its make, model, original purchase price, and estimated replacement cost. If you have the data, include the date of purchase.

For damaged items, provide an estimated repair cost. Total all losses at the bottom. The goal is to provide a comprehensive financial assessment.

6. The Concluding Summation: Formalities and Call to Action

End your letter with a formal closing. Use “Sincerely,” or “Respectfully,” followed by your full name, address, phone number, and email address. Clearly state the action you anticipate from the insurer.

This will keep things on track. Acknowledge your preparedness to assist them with any further inquiries. This creates a sense of willing cooperation and streamlines the claims process.

7. Polishing and Dispatch: Editing and Submission

Before sending, review the entire letter. Proofread for any grammatical errors or spelling mistakes. Ensuring clarity is paramount. Send the letter via certified mail with return receipt requested.

This provides you with proof of delivery. Keep a copy of the letter, all attachments, and the return receipt for your records. This creates an organized audit trail.

FAQs about Explanation Letter for Break in Homeowners Insurance

What is an Explanation Letter for a Break in Homeowners Insurance and Why is it Needed?

An Explanation Letter for a break in homeowners insurance is a document you send to your insurance provider to clarify why there was a lapse in your coverage. This letter is crucial because a break in coverage can potentially affect your eligibility for future claims and the premiums you pay.

The purpose is to provide context and demonstrate that the lapse was due to circumstances beyond your control, or that you have taken steps to rectify the situation and maintain adequate coverage going forward.

What Information Should I Include in My Explanation Letter?

Your letter should clearly state the period of the coverage lapse. Explain the specific reason for the break in coverage, be it a missed payment, a change of address, or any other factor.

Provide supporting documentation if available. Include the date of the lapse and the date the coverage was reinstated or when you intend to reinstate it. If applicable, mention any steps you have taken to prevent a recurrence, such as setting up automatic payments. Finally, be sure to include your policy number, your name, address and contact information for clarity.

What Happens if I Don’t Provide an Explanation Letter?

If you fail to provide an explanation letter, your insurance provider might deny future claims related to events that occurred during the coverage lapse.

They may also consider the lapse a higher risk, which could lead to increased premiums. Additionally, it could make it difficult or more expensive to obtain future insurance coverage with the same or different insurers. It is always in your best interest to communicate proactively with your insurance provider to avoid these potential complications.

Can Circumstances Beyond My Control Be Used to Justify a Coverage Lapse?

Yes, your letter should clearly explain that the coverage lapse was due to factors outside of your control, such as a billing error, unforeseen financial hardship, a natural disaster, or a mistake on the part of your previous insurance company.

When possible, include proof, such as bank statements, medical bills, or any communication with your previous insurer. Documentation strengthens your case and increases the likelihood that your insurance company understands and shows leniency.

How Can I Prevent Future Lapses in Homeowners Insurance Coverage?

To prevent future lapses, consider setting up automatic payments for your premiums to ensure timely payment. Keep your contact information current with your insurance provider so that you receive all billing notices and policy updates.

Review your policy regularly and understand the terms and conditions. If you anticipate any changes to your financial situation or address, notify your insurer immediately. Most importantly, maintain open communication with your insurance provider.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study