Dealing with an insurance company can be tough. Sometimes, you get an unfair settlement. This is where a dispute letter for unfair insurance settlement comes in. It’s a formal way to challenge the insurance company’s offer. The purpose? To try to get a better payout that covers your actual losses.

This article can make the whole process easier. We’re offering dispute letter for unfair insurance settlement templates. You can use them to write your own letter. Need a sample dispute letter for insurance claim denial? We’ve got it. We also have other examples.

Our goal? To simplify your life. Writing these letters can be stressful. Our dispute letter examples will save you time and effort. We want to empower you. Good luck with your insurance settlement dispute!

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

Subject: Dispute of Unfair Insurance Settlement – Policy Number [Your Policy Number]

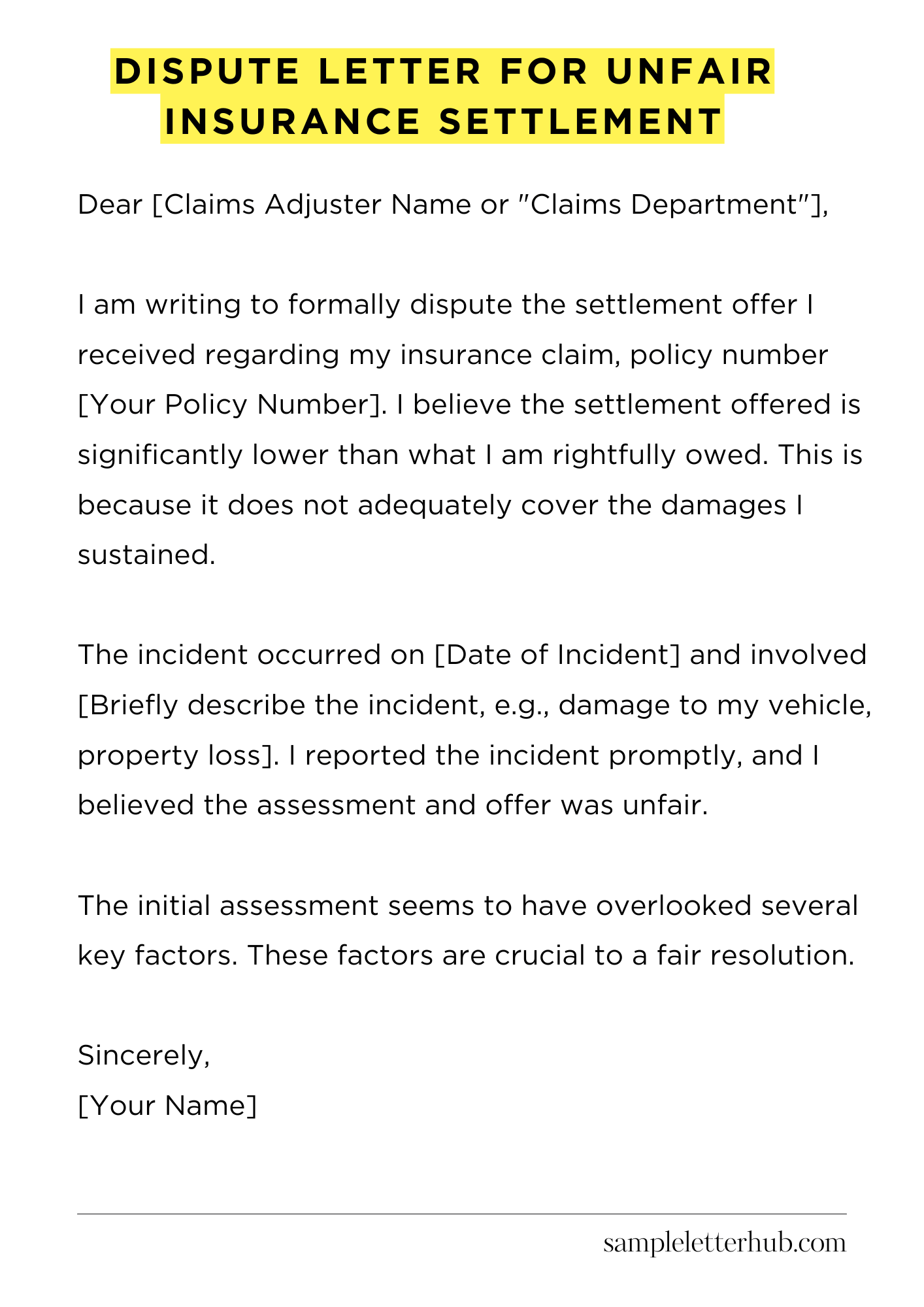

Dear [Claims Adjuster Name or “Claims Department”],

I am writing to formally dispute the settlement offer I received regarding my insurance claim, policy number [Your Policy Number]. I believe the settlement offered is significantly lower than what I am rightfully owed. This is because it does not adequately cover the damages I sustained.

The incident occurred on [Date of Incident] and involved [Briefly describe the incident, e.g., damage to my vehicle, property loss]. I reported the incident promptly, and I believed the assessment and offer was unfair. The initial assessment seems to have overlooked several key factors. These factors are crucial to a fair resolution.

Specifically, the settlement offer undervalues [Mention specific items, e.g., the cost of repairs, the replacement value of damaged items, medical expenses]. Furthermore, the depreciation calculation appears to be inaccurate.

It also appears the adjuster did not consider [Mention specific issues with the assessment]. I provided documentation in my initial claim, to support my claim of the full cost of the loss.

I have attached [Mention any documents you are including, e.g., estimates, receipts, photographs]. These documents further illustrate the extent of the damages and the associated costs. Please review them carefully.

I am seeking a revised settlement offer that reflects the true cost of my losses. This should consider all the damages. I would like a settlement that covers everything. I am confident that a fair assessment will lead to a more equitable resolution.

I would appreciate it if you could reconsider my claim and provide me with a revised offer within [Number] days. Please contact me at your earliest convenience to discuss this matter further. I am available at the phone number listed above. You can also reach me by email.

Thank you for your time and attention to this important matter. I look forward to your prompt response.

Sincerely,

[Your Name]

How to Write Dispute Letter for Unfair Insurance Settlement

Receiving an insurance settlement that seems inequitable? You’re not alone. Many individuals find themselves in this predicament. Don’t simply accept the insurer’s initial offer. You possess the agency to dispute it. This guide will walk you through crafting a compelling dispute letter, helping you advocate for a fairer resolution.

1. Comprehend the Premise of Your Grievance

Before you begin penning your letter, gain a comprehensive understanding of the reasons behind your dissatisfaction. Scrutinize the insurance company’s valuation. Identify specific elements you believe are undervalued or overlooked.

Perhaps they underestimated repair costs, medical expenses, or the overall impact of the incident. Note these incongruities; this is the genesis of your argument.

2. Gather the Requisite Supporting Documentation

A well-written letter must be supported by irrefutable evidence. Assemble all pertinent documents. This could encompass medical bills, repair estimates, police reports, photographs of the damage, and any correspondence exchanged with the insurance company.

This collection serves as your epistolary ammunition, bolstering your claims and solidifying your position. Organize everything; it is a critical step in the process.

3. Structuring Your Dispute Letter: The Anatomy

Your dispute letter needs a clear and concise structure. Here is how you can formulate one.

- Salutation: Begin formally. Use “Dear Claims Adjuster” or the adjuster’s name if known.

- Identification: Clearly state your name, the claim number, and the date of the incident.

- Statement of Disagreement: Concisely explain why you’re disputing the settlement. Be direct.

- Specific Grievances: Detail each area of disagreement, citing evidence from your documentation. Use numbered points for clarity.

- Requested Remedy: Explicitly state what you are seeking (e.g., an increased settlement amount).

- Closing: Reiterate your desire for a fair resolution. Include your contact information.

- Signature: Sign the letter. Print your name below.

4. The Eloquence of Your Prose: Crafting the Content

The language you employ is crucial. Maintain a professional and courteous tone, even if you are frustrated. State the facts objectively. Refrain from using emotionally charged language. Be specific and precise in your claims. Avoid rambling or irrelevant information. Clarity and conciseness are paramount.

5. Deciphering the Art of Persuasion

Your goal is to convince the insurance company to reconsider their initial offer. Emphasize the validity of your claims with supporting evidence. Highlight the financial impact of the incident. If applicable, cite relevant insurance policy provisions that support your position. Demonstrate that you have diligently researched your claim and are fully informed.

6. The Art of Delivery: Transmitting Your Letter

How you submit your letter is important. Always send your dispute letter via certified mail with return receipt requested. This provides proof of delivery and ensures the insurance company receives your communication. Keep a copy of the letter, all supporting documents, and the return receipt for your records. This is vital in case further action is needed.

7. What Happens After You Submit: Post-Submission Protocol

Once you dispatch the letter, patiently await the insurer’s response. Understand that it may take some time for them to review your case. Keep a record of all correspondence and conversations. If the initial response is unsatisfactory, you may need to escalate the matter.

This may involve filing a complaint with your state’s insurance commission or, as a last resort, seeking legal counsel. Remain steadfast in your pursuit of a fair resolution.

FAQs about Dispute Letter for Unfair Insurance Settlement

What is a dispute letter for an unfair insurance settlement, and why is it necessary?

A dispute letter, also known as a demand letter, is a formal written communication sent to an insurance company to challenge their settlement offer.

It is necessary when you believe the offered settlement is insufficient to cover your losses, damages, or injuries resulting from an insured event. The letter outlines your reasons for disagreement, presents evidence supporting your claim, and demands a more reasonable settlement amount.

What information should I include in a dispute letter?

A comprehensive dispute letter should include the following: your identifying information (name, address, policy number), the date of the incident, a clear description of the incident and resulting damages, the initial settlement offer and why it is deemed unfair, detailed documentation supporting your claim.

What kind of evidence is helpful to include with my dispute letter?

Include any evidence that supports your claim and validates your damages. This may include, but is not limited to: Police reports, medical records and bills, photographs or videos of the damage, repair estimates, lost wage documentation, expert opinions (e.g., from doctors or engineers).

What happens after I send a dispute letter?

After sending the dispute letter, the insurance company will review your claim and the supporting documentation. They may contact you for further information or clarification.

The insurance company can respond in several ways: by increasing their settlement offer, denying your claim, or maintaining their original offer. You should monitor their response time as well as any deadlines you include in your letter.

Depending on their response, you may need to negotiate further, pursue mediation, or consider legal action if a satisfactory resolution is not reached.

When is it advisable to seek legal counsel regarding an unfair insurance settlement?

It’s advisable to seek legal counsel if: the insurance company is unresponsive or refuses to negotiate in good faith, the settlement offer is significantly lower than your assessed damages, the insurance company denies your claim without a valid reason, the case involves complex legal issues or significant financial losses.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study