Dealing with a rejected property damage claim can be frustrating. A dispute letter for rejected property damage claim is your formal way of fighting back. It tells the insurance company why you disagree. This letter lays out your case, highlighting the reasons for the denial. Its main purpose is to convince the insurer to reconsider their decision.

We get it. Writing a strong dispute letter isn’t always easy. To help, we have created something special for you. We will share a bunch of templates. These templates are like building blocks. They help you craft a persuasive sample dispute letter.

Our property damage claim dispute letter samples are tailored for various situations. You’ll find examples to address common rejection reasons. Use these dispute letter examples to save time and effort. Write your own powerful letter with ease.

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

Subject: Dispute of Rejected Property Damage Claim – Policy Number [Your Policy Number]

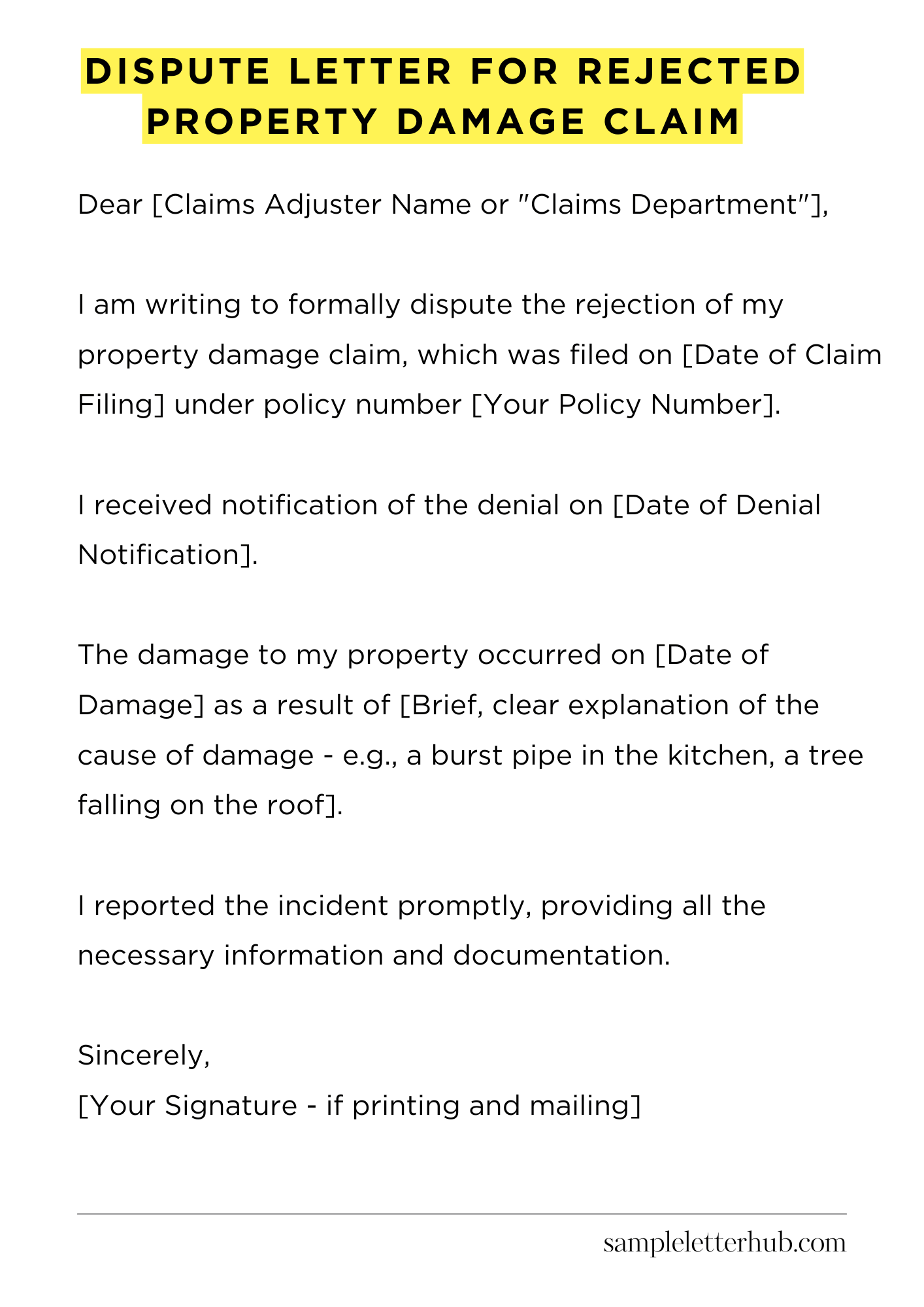

Dear [Claims Adjuster Name or “Claims Department”],

I am writing to formally dispute the rejection of my property damage claim, which was filed on [Date of Claim Filing] under policy number [Your Policy Number]. I received notification of the denial on [Date of Denial Notification]. This letter explains why I believe the denial is incorrect and why my claim should be reconsidered.

The damage to my property occurred on [Date of Damage] as a result of [Brief, clear explanation of the cause of damage – e.g., a burst pipe in the kitchen, a tree falling on the roof].

I reported the incident promptly, providing all the necessary information and documentation, including [List key documents you provided – e.g., photographs, repair estimates, police report]. The damage caused significant distress.

The reason provided for the denial was [State the reason for denial as stated by the insurance company – e.g., lack of coverage, pre-existing condition]. However, I believe this reason is inaccurate because [Clearly and concisely explain why you disagree with the reason for denial. Provide evidence to support your claim].

For example, the policy specifically states [Quote the relevant section of your policy]. I feel that the policy does indeed cover this event.

I have attached [List any new documents you are including with the letter – e.g., additional photographs, updated repair estimates, a statement from a professional]. These documents further support my claim and demonstrate the extent of the damage and the associated costs. I have provided the estimates here.

I believe my claim should be approved, and I am requesting a thorough review of my case. I am confident that upon reviewing the information, you will find my claim to be valid. I look forward to your prompt response and a positive resolution to this matter. Please contact me at your earliest convenience to discuss this further.

Sincerely,

[Your Signature – if printing and mailing]

How to Write Dispute Letter for Rejected Property Damage Claim

A property damage claim denial can be a frustrating experience. But, understanding how to navigate the process of contesting that denial with a compelling dispute letter is crucial. This guide provides a practical roadmap.

1. Commence with Conciseness: Your Salutation and Initial Statement

Begin your letter with a professional salutation. Use “Dear [Insurance Adjuster’s Name]” or if unknown, “Dear Claims Adjuster.” Immediately after, state your intention.

Clearly indicate you are disputing the denial of your property damage claim. Identify your policy number, the date of the incident, and the initial claim number assigned by the insurer. Don’t beat around the bush; clarity is your ally here.

2. The Art of Recapitulation: Summarizing the Event and Claim

Briefly and objectively summarize the incident leading to the damage. This should be a concise recap of the events, not a verbose narrative. Reference any supporting documentation you initially provided. Include details such as the date, time, and specific location of the damage. This re-establishes the factual basis of your claim, reinforcing its validity in the reader’s mind.

3. Deconstructing the Denial: Addressing the Insurer’s Rationale

Carefully review the rejection letter from your insurer. Identify each reason cited for the denial. Objectively address each point. Dissect their logic. If the denial hinges on a specific exclusion, explain why you believe that exclusion does not apply to your situation. This is where you challenge the basis of their decision.

4. Assemble Your Arsenal: Gathering and Presenting Evidence

Compile all supporting evidence. This might include: photos, videos, repair estimates, witness statements, and any other relevant documentation that substantiates your claim. Present the evidence in a logical manner, cross-referencing it to the insurer’s reasons for denial. Focus on linking your evidence to rebutting their assertions. Make their denial look flimsy.

5. Deciphering the Policy: Highlighting Pertinent Policy Language

Carefully analyze your insurance policy. Quote and highlight specific policy language that supports your claim. This is where you demonstrate how the terms of your policy mandate coverage for the damages you suffered. Emphasize any ambiguities in the policy wording that might favor your interpretation. Use legal language only if necessary.

6. A Plea for Reconsideration: The Call to Action

Clearly state what you expect from the insurer. Request that they reconsider their decision and approve your claim. Be specific about the desired outcome, whether it’s full coverage or a revised settlement. Provide a reasonable timeframe for their response. End with a professional closing. Use a courteous tone.

7. The Final Flourish: Formalities and Follow-Up

Conclude your letter with a professional closing, such as “Sincerely” or “Respectfully.” Sign the letter and print your name clearly. Include your contact information.

Make a copy of the letter and all supporting documentation for your records. Consider sending the letter via certified mail with a return receipt requested to provide proof of delivery. Follow up with the insurer if you do not receive a timely response. Don’t be afraid to escalate the matter if necessary.

FAQs about Dispute Letter for Rejected Property Damage Claim

What is a dispute letter for a rejected property damage claim, and why is it important?

A dispute letter is a formal communication sent to an insurance company contesting the denial of a property damage claim. It’s crucial because it’s your primary means of challenging the insurer’s decision, providing additional evidence, and potentially securing the compensation you’re entitled to.

It serves as an official record of your disagreement and initiates the process for a review or potential reconsideration of the claim.

What information should I include in a dispute letter?

Your dispute letter should clearly identify the claim, policy number, and the reason for the rejection as stated by the insurance company. Include a detailed explanation of why you disagree with their decision, providing specific facts and evidence (photos, videos, repair estimates, witness statements, etc.) to support your claim.

Reference relevant policy provisions, and state the specific outcome you’re seeking (e.g., payment for repairs). Keep it concise, organized, and professional.

What are the common reasons for property damage claims being rejected?

Common reasons include insufficient evidence of damage, pre-existing damage, policy exclusions (e.g., acts of nature, specific perils), failure to comply with policy terms (e.g., timely reporting), or the insurer’s belief that the damage wasn’t caused by a covered event. Understanding the stated reason for denial is crucial to effectively address it in your dispute letter.

What is the timeframe for submitting a dispute letter, and what happens after I send it?

Check your insurance policy for specific deadlines for appealing a denied claim. Failing to meet deadlines can result in the loss of your right to appeal. After sending the letter, the insurance company typically reviews your submission, assesses the new information, and may request additional documentation.

They will then send a response, which can range from a denial reaffirmation to a partial or full approval of your claim. Be sure to keep records of all communications.

When should I consider seeking legal advice regarding my disputed claim?

If your claim involves a significant amount of money, the denial seems unfair or unjustified, the insurance company is unresponsive or acting in bad faith, or if you’re unfamiliar with insurance regulations or legal procedures, it’s wise to consult with an attorney specializing in insurance disputes.

Legal counsel can evaluate your case, advise you on your rights, and represent you in negotiations or litigation, if necessary.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study