A clarification letter to an insurance company is a formal document. Its purpose is to get more information. You can use it to clear up any confusion. It clarifies details about your insurance policy or insurance claim. This helps ensure everything is understood correctly.

Need to write your own insurance clarification letter? We’ve got you covered. This article offers helpful letter templates. You’ll find plenty of examples and samples. Use these to craft your perfect letter.

Whether you need a sample letter for insurance claim clarification or any other insurance-related letter, we make it easy. We provide a variety of formats. We’ll show you exactly what to write. Make the process much simpler!

[Your Name/Your Company Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

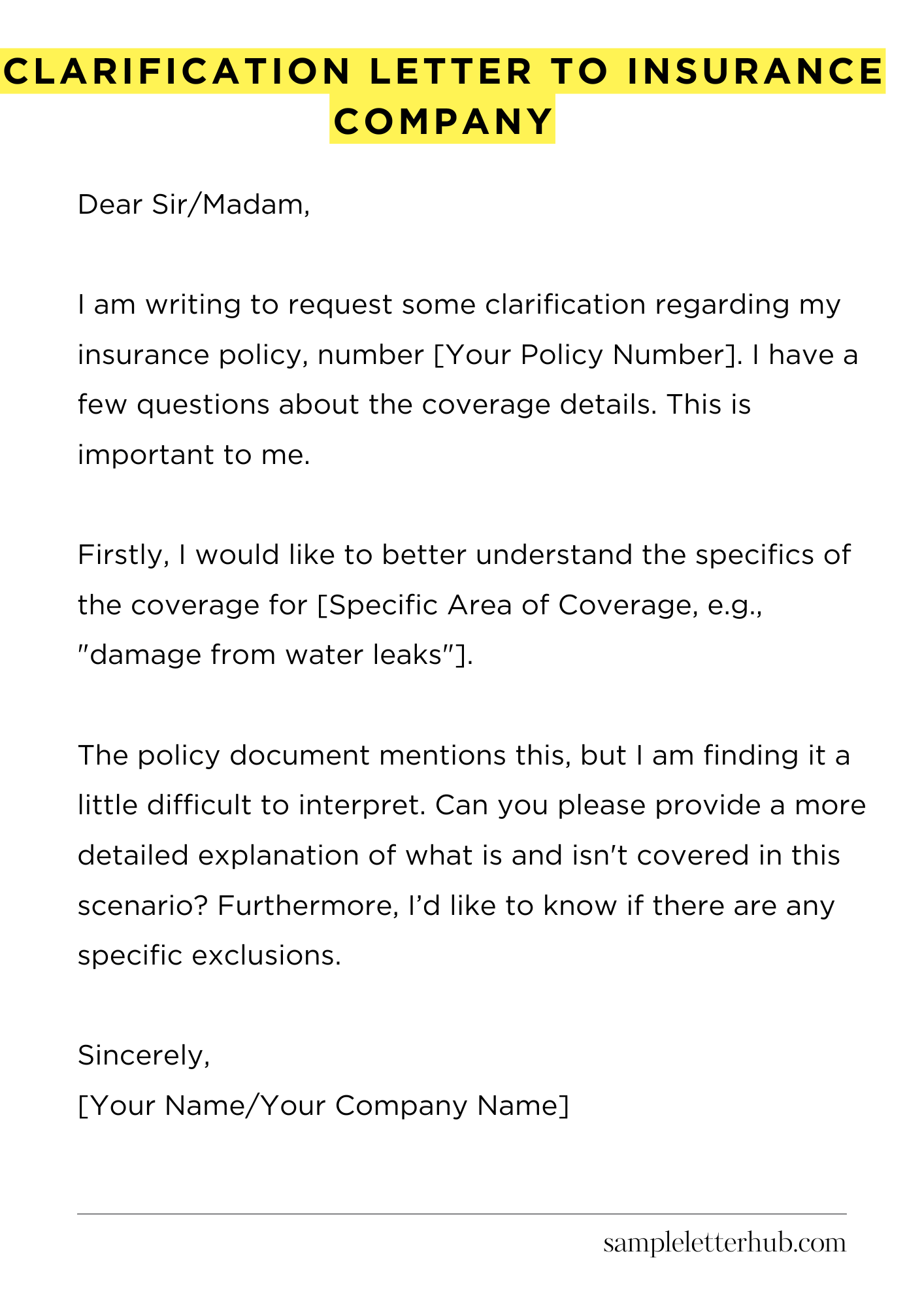

Subject: Clarification Regarding Policy Number [Your Policy Number]

Dear Sir/Madam,

I am writing to request some clarification regarding my insurance policy, number [Your Policy Number]. I have a few questions about the coverage details. This is important to me.

Firstly, I would like to better understand the specifics of the coverage for [Specific Area of Coverage, e.g., “damage from water leaks”].

The policy document mentions this, but I am finding it a little difficult to interpret. Can you please provide a more detailed explanation of what is and isn’t covered in this scenario? Furthermore, I’d like to know if there are any specific exclusions.

Secondly, I’m hoping to have confirmation on the process for filing a claim under [Another Specific Area of Coverage, e.g., “medical expenses”]. What documents are required, and what is the typical turnaround time for claim processing? It’s good to be prepared.

Finally, could you clarify the deductible amount applicable to [Specific Type of Claim, e.g., “wind damage”]? I want to make sure I understand my responsibilities should I ever need to file a claim of that nature. It is crucial to me.

I would appreciate it if you could respond to these questions at your earliest convenience. I am looking forward to receiving your response. You can reach me at the phone number or email address listed above. I appreciate your assistance in this matter. Thank you for your time.

Sincerely,

[Your Name/Your Company Name]

How to Write a Clarification Letter to an Insurance Company

Navigating the byzantine labyrinth of insurance claims can feel like traversing a legal minefield. Sometimes, a denial or a request for more information is received, and a clarification letter becomes your essential tool.

Crafting a concise and persuasive letter can often be the crucial element in securing a favorable outcome. This guide will help you construct a compelling clarification letter, maximizing your chances of success.

1. Comprehend the Quandary

Before you even put pen to paper (or fingers to keyboard), thoroughly understand the insurance company’s query or denial. Carefully review all documentation, including the denial letter itself.

Identify the specific points of contention or the additional information they require. Deconstruct the issue. Pinpoint the precise reason for their hesitation. The clarity of your response hinges on your grasp of their concerns.

2. Gather Your Ammunition: The Supporting Documentation

A well-supported argument is always more potent. Assemble all relevant documentation. This might include medical records, police reports, receipts, witness statements, and any other evidence that bolsters your claim.

Organize these documents meticulously. Ensure they are easily referenced and clearly labelled. Consider sending copies, and always retain the originals for your records. This is your arsenal; wield it effectively.

3. The Salutation and Introductory Prolegomenon

Begin with a professional salutation. Use “Dear Claims Adjuster,” or “Dear Sir/Madam,” followed by the adjuster’s name if known. In the introductory paragraph, succinctly state the purpose of your letter.

Reference the claim number and date of the initial filing. Briefly outline the subject matter you are addressing. Frame your intent right from the outset.

4. Address the Specific Contentions with Precision

This is the heart of your letter. Address each point of concern raised by the insurance company individually. Provide clear, concise, and factual responses to each question or objection.

Refer to the supporting documentation you have gathered, citing specific page numbers or dates. Avoid ambiguous language. Be direct. Stick to the facts. Don’t engage in emotional rhetoric; it undermines your credibility. Maintain a detached tone.

5. The Art of Persuasion: Crafting Your Argument

While maintaining a factual tone, subtly weave in persuasive elements. Frame your responses in a way that aligns with the policy’s terms and conditions. Highlight any clauses or provisions that support your claim.

Explain why the denial or request for information is inaccurate or unwarranted. Use logical reasoning and a clear chain of thought to build a compelling case. Demonstrate how your claim is unequivocally covered.

6. The Concluding Admonition and Sign-off

In the concluding paragraph, summarize your key points and reiterate your request for coverage. Express your desire for a prompt resolution. State what action you expect the insurer to take.

Provide your contact information, including your phone number and email address. Sign the letter formally. Always retain a copy of the letter and all attachments for your records. Maintain the documentary trail of everything.

7. Polishing the Lexicon: Proofreading and Delivery

Before sending, meticulously proofread your letter. Check for grammatical errors, typos, and factual inaccuracies. Ensure the language is clear, concise, and professional.

Consider having a second pair of eyes review the letter for clarity and accuracy. Send the letter via certified mail with a return receipt requested. This provides proof of delivery and ensures you have a record of when the insurance company received your response. Now, submit your letter with confidence.

FAQs about Clarification Letter to Insurance Company

What is a clarification letter to an insurance company?

A clarification letter to an insurance company is a formal written communication used to address ambiguities, request further details, or seek explanations regarding a specific aspect of your insurance policy, claim, or related correspondence. It aims to clear up any confusion and ensure a mutual understanding between you and the insurance provider.

When should I send a clarification letter?

You should send a clarification letter whenever you encounter unclear terms, confusing language, discrepancies in documents, or a lack of specific information in your insurance-related communications.

This could be after receiving a policy document, claim denial, Explanation of Benefits (EOB), or any communication that leaves you with unanswered questions or concerns.

What information should be included in a clarification letter?

A comprehensive clarification letter should include your policy information (policy number, insured name, etc.), the date of the original document or communication you are referring to, a clear and concise explanation of the issues needing clarification, specific questions, and any relevant supporting documents.

How should I format and send a clarification letter?

Format your letter professionally, using a clear and concise tone. Include the date, your name and address, and the insurance company’s address. Clearly state the purpose of the letter in the subject line.

Send the letter via certified mail with return receipt requested to maintain a record of delivery. Keep a copy of the letter and proof of mailing for your records.

What happens after I send a clarification letter?

After sending a clarification letter, the insurance company should respond, typically within a specific timeframe outlined in your policy or state regulations. The response should address your questions and concerns directly.

If you are not satisfied with the response, you may need to follow up, escalate the issue to a higher level within the company, or seek assistance from your state’s insurance regulatory agency or an attorney.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study