Ever received an insurance bill that just didn’t seem right? A “Letter to Fix Mistake in Annual Premium Amount” is your tool to address those billing errors. It’s a formal way to notify your insurance provider about discrepancies in your premium. The goal is to get the correct amount charged and avoid overpaying.

We understand navigating insurance can be confusing. That’s why we’ve prepared examples and samples of Letter to Fix Mistake in Annual Premium Amount. Our focus is to simplify the process. These letter templates will guide you. Writing the perfect letter to dispute insurance premium is now easier than ever.

We’ve got you covered with a variety of formats. Find a sample letter that suits your specific situation. This article will help you create a letter for premium adjustment. Get ready to correct those billing mistakes!

[Your Name/Your Company Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

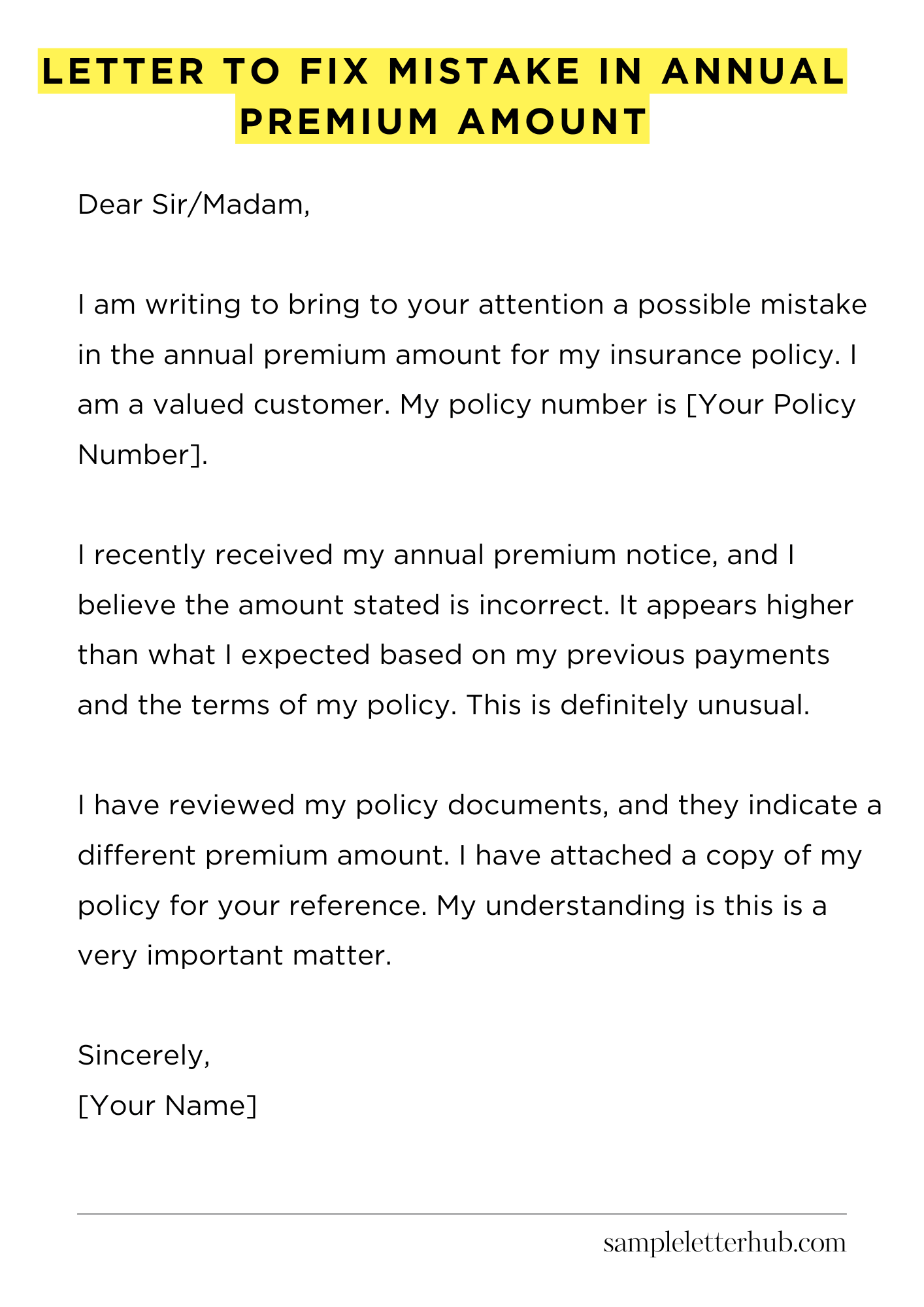

Dear Sir/Madam,

I am writing to bring to your attention a possible mistake in the annual premium amount for my insurance policy. I am a valued customer. My policy number is [Your Policy Number].

I recently received my annual premium notice, and I believe the amount stated is incorrect. It appears higher than what I expected based on my previous payments and the terms of my policy. This is definitely unusual.

I have reviewed my policy documents, and they indicate a different premium amount. I have attached a copy of my policy for your reference. My understanding is this is a very important matter.

Could you please investigate this matter and clarify the discrepancy? I would appreciate it if you could review the details of my policy. Please compare the stated amount with the documentation.

I would also appreciate it if you could inform me of the reason for the difference, if any. Getting an explanation would be very helpful. I would also like to know how the issue will be corrected.

I look forward to your prompt response and resolution to this matter. This situation needs to be resolved quickly. Thank you for your time and attention to this important issue.

Sincerely,

[Your Name]

How to Write Letter to Fix Mistake in Annual Premium Amount

Encountering an error in your annual premium amount can be frustrating, but rectifying it is often a straightforward process. A well-crafted letter can be your most potent tool in this situation.

It serves as your formal conduit to communicate the discrepancy, document your concerns, and initiate a resolution. Here’s a comprehensive guide to composing a compelling letter to address this issue, ensuring clarity and efficacy.

1. Commence with Precision: Your Formal Salutation and Addressee

Begin your missive with a professional and respectful salutation. If you know the name of the specific insurance agent or representative, address them directly (e.g., “Dear Ms. Johnson”).

If not, use a general greeting such as “Dear Insurance Provider,” or “To Whom It May Concern.” This immediately establishes a tone of formality. Always include the insurance company’s official address.

2. The Core Tenets: Identify the Policy and State the Error

The core of your letter should unambiguously state your policy details and the precise nature of the error. Clearly identify your policy number, the name of the insured, and the date of the annual premium statement. Provide a succinct and verifiable description of the discrepancy.

For instance, instead of saying, “The amount is wrong,” state: “The annual premium listed on statement dated October 26, 2023, is $2,000, whereas the correct premium, based on my policy terms, should be $1,800.” Be specific, precise and clear.

3. Provide Substantiation: Your Supporting Evidence

This is where your letter transforms from a complaint to a compelling argument. Attach copies of supporting documentation to validate your claim.

This might include your original policy documents, previous premium statements, payment receipts, or any other paperwork that corroborates your version of the correct premium. Reference these attachments in your letter, such as: “Attached, please find a copy of my policy, which clearly outlines the premium calculation.” This strengthens your claim and enables prompt verification.

4. Articulate Your Desired Outcome: The Specific Request

Be explicit about the action you want the insurance provider to take. Do you want them to correct the amount and issue a revised statement? Request a refund for the overpayment?

State precisely what resolution you are seeking. For example, “I request that you investigate this discrepancy and adjust my premium to the correct amount. I would also appreciate a refund of the overpayment of $200.” Don’t beat around the bush; be direct and concise.

5. Establish a Timeline: Setting Expectations

While you may not be privy to their internal procedures, it is still crucial to set a time bound expectation to receive a response. Provide a reasonable timeframe for the insurance provider to respond.

Suggest a window like, “I would appreciate a response and the correction of this error within thirty days of the date of this letter.” This sets a clear expectation and adds a sense of urgency.

6. The Formal Closure: Gratitude and Contact Information

Conclude your letter with a professional closing, such as “Sincerely” or “Respectfully.” Provide your full name, address, phone number, and email address. This ensures they can easily contact you for clarification or confirmation. Your contact details offer convenient avenues of communication.

7. Final Precaution: Keeping a Copy and Sending Methods

Before mailing your letter, make a copy for your records. This is vital for tracking purposes. When sending your letter, consider using certified mail with return receipt requested.

This provides proof that the letter was received and when. For electronic communications, request a read receipt if you send via email. This guarantees a traceable history of your correspondence.

FAQs about Letter to Fix Mistake in Annual Premium Amount

What is the purpose of a letter to fix a mistake in the annual premium amount?

The primary purpose of a letter to fix a mistake in the annual premium amount is to formally notify an insurance company or financial institution about an error in the initially billed or quoted premium. This letter serves as a documented request for correction, ensuring that the premium amount reflects the accurate terms of the policy or agreement.

What information should be included in a letter to correct the annual premium amount?

A comprehensive letter should include the policy or account number, the date of the error, a clear description of the mistake (e.g., incorrect coverage level, wrong calculation, overlooked discount), the correct premium amount, supporting documentation (if applicable, such as a copy of the policy or a previous quote).

What type of supporting documentation might be needed when requesting a premium correction?

Depending on the nature of the error, supporting documentation can vary. Examples include a copy of the original policy document, prior quotes, any written communication that supports the correct premium, or proof of eligibility for a discount (e.g., proof of association membership). The specific documentation required will depend on the cause of the discrepancy.

How should the letter to correct the annual premium amount be delivered?

The method of delivery should ensure proof of receipt. Certified mail with return receipt requested is a secure option. Other acceptable methods include email (if the company provides a specific address for such requests), or through a secure online portal (if available). Always retain a copy of the letter and any supporting documents for your records.

What steps should be taken if the insurance company denies the request to correct the premium?

If the insurance company denies the request, the policyholder should first review the denial letter carefully to understand the reason. Further steps may include gathering additional supporting documentation, escalating the issue to a supervisor or the company’s internal dispute resolution process.

Depending on the situation, the policyholder can also consider filing a complaint with the state’s insurance regulatory agency or seeking legal counsel.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study

Resignation letter due to long commute