You’ve likely paid for insurance. Sometimes, your insurance company might downgrade your policy. This means the coverage changes, often for less protection. A premium refund request due to policy downgrade is how you ask for money back. It aims to get a refund for the unused portion of your premium.

Dealing with insurance can be tricky. Writing the perfect premium refund request can be challenging. We get it. That’s why we’re here to help. This article provides helpful examples. We’ll share premium refund request letter templates and samples to guide you.

Our goal is simple. We want to make it easier for you. You’ll find different formats. We offer various scenarios. Each premium refund request will be crafted to address policy downgrade situations. Get ready to write a strong request letter today!

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

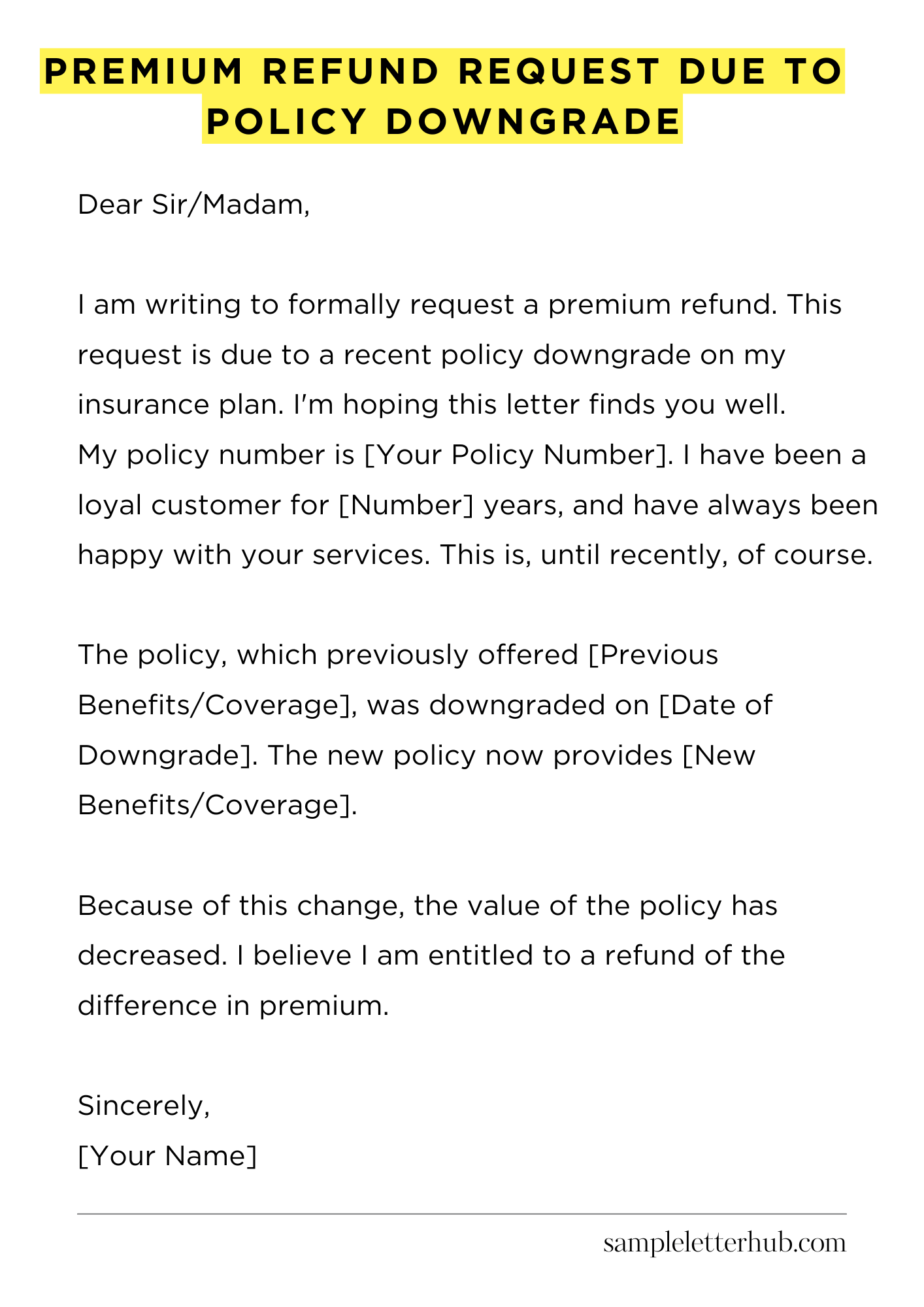

Dear Sir/Madam,

I am writing to formally request a premium refund. This request is due to a recent policy downgrade on my insurance plan. I’m hoping this letter finds you well.

My policy number is [Your Policy Number]. I have been a loyal customer for [Number] years, and have always been happy with your services. This is, until recently, of course.

The policy, which previously offered [Previous Benefits/Coverage], was downgraded on [Date of Downgrade]. The new policy now provides [New Benefits/Coverage]. The reduction in benefits is quite significant.

Because of this change, the value of the policy has decreased. I believe I am entitled to a refund of the difference in premium. The premium I am currently paying does not align with the reduced coverage I now receive. This is a matter of fairness.

I would appreciate it if you would review my request and process the appropriate refund. Please let me know the amount of the refund. It’s important to me that this be addressed quickly.

I have attached copies of both my original policy document and the updated policy document for your reference. These documents should help speed up the process.

Please contact me at your earliest convenience to confirm receipt of this letter and to discuss the next steps. Thank you for your time and attention to this matter. I look forward to hearing from you soon.

Sincerely,

[Your Name]

How to Write Premium Refund Request Due to Policy Downgrade

A policy downgrade can be a frustrating experience, especially when it affects your coverage and necessitates a reconsideration of your financial outlay. Fortunately, a well-crafted refund request can often remedy this situation.

This guide will meticulously walk you through the process of formulating a persuasive and effective request for a premium refund due to a policy downgrade.

1. Scrutinize the Policy Documentation

Before you even think about penning your request, perform a comprehensive exegesis of your policy documents. Carefully examine the clauses pertaining to policy modifications, downgrades, and premium adjustments.

Look for specific language related to refunds or proportional returns of premium upon a downgrade. This initial reconnaissance is critical, as it will serve as the bedrock of your argument, allowing you to cite specific policy sections in your letter.

2. Gather Pertinent Information

Compile all relevant information. This includes your policy number, the date the downgrade took effect, the original premium, the new premium, and the precise nature of the downgrade.

Ascertain the dates of any communications regarding the downgrade and the details of any prior discussions you’ve had with the insurance provider. Precise record-keeping is paramount here; it strengthens the veracity of your claim.

3. Structure Your Refund Request

Your refund request must be structured logically. Start with a polite salutation and clearly state your purpose: to request a refund due to a policy downgrade.

Then, unequivocally state the policy number and the effective dates involved. Detail the specifics of the downgrade, explicitly outlining how it has diminished your coverage or altered your benefits. Support your claims with concrete evidence and policy citations. Be direct and avoid ambiguity. This will help you to get a positive response.

4. Articulate Your Rationale

This is where you build your case. Clearly explain why you believe a refund is warranted. You might argue that the downgrade was not communicated sufficiently, that the reduced coverage no longer meets your needs, or that the premium reduction is not commensurate with the decrease in benefits.

If applicable, allude to any promises or misrepresentations made during the initial policy sale. Focus on the impact the downgrade has had on you. Make it clear. This will make your request strong.

5. Present Your Desired Outcome

Clearly state the refund amount you are requesting or the method by which you would like the refund to be calculated (e.g., a pro-rata refund for the period of the downgrade).

If the policy allows, and you are amenable, consider requesting a credit towards a future policy or the reinstatement of the original coverage. Be specific and reasonable. The clearer your request, the less room there is for misinterpretation.

6. Ensure Clarity and Professionalism

Maintain a professional tone throughout your letter. Use formal language and avoid slang or emotional outbursts. Proofread meticulously for any grammatical errors or typographical slip-ups.

Your credibility hinges on the clarity and professionalism of your communication. Remember, a polished letter reflects your seriousness and increases the likelihood of a favorable response.

7. Submission and Follow-up

Send your letter via certified mail with a return receipt requested. This provides proof of delivery and ensures you have a record of the date the insurance provider received your request.

Retain a copy of the letter for your records. If you do not receive a response within a reasonable timeframe (typically 30 days), follow up with a phone call or a second, slightly more assertive letter. Persistently pursue your claim until a resolution is reached.

FAQs about Premium Refund Request Due to Policy Downgrade

How is a policy downgrade defined, and what situations typically trigger it?

A policy downgrade refers to a change in your insurance coverage that reduces the benefits, coverage limits, or overall value of your policy. This can happen for various reasons, including changes in eligibility, a shift in risk assessment by the insurer, or alterations to the terms and conditions of the policy.

Common scenarios that trigger downgrades include a change in the insured’s health status (for health or life insurance), a change in the use of a property (for home insurance), or the insurer’s decision to alter coverage options for a specific product.

What are the specific grounds for requesting a premium refund following a policy downgrade?

Grounds for a premium refund typically arise when a policy is downgraded, and the premium paid no longer accurately reflects the reduced coverage. This is often the case when the downgrade results in a lower level of benefits, a higher deductible, or a reduction in the scope of covered risks.

The specific terms for a refund, if any, will be outlined in the policy documents, which should be reviewed carefully. Pro-rata refunds are common, meaning the refund is calculated based on the unused portion of the premium for the remaining policy term.

What documentation is needed to support a premium refund request related to a policy downgrade?

Supporting documentation is crucial for a successful refund request. This usually includes a copy of the original insurance policy, any correspondence related to the policy downgrade (such as a notice from the insurer), and proof of premium payments (e.g., bank statements, receipts).

You may also be required to provide documentation explaining the reasons for the downgrade, especially if the downgrade was based on information you provided or a change in circumstances. It is important to keep records of all communications with the insurer.

How is the refund amount calculated in the event of a policy downgrade?

The calculation of a refund amount depends on the specific terms of the policy and the nature of the downgrade. Typically, the insurer will calculate the difference between the premium paid and the premium that would have been charged for the downgraded coverage during the period the lower coverage was in effect.

This calculation may also be pro-rata based on the remaining term of the policy after the downgrade. The policy documents will usually provide the specific method for calculation.

What is the typical process for submitting a premium refund request, and how long does it usually take to receive the refund?

The process for submitting a refund request typically involves contacting the insurance provider’s customer service department or submitting a formal request in writing. The specific method may be outlined in the policy documentation or on the insurer’s website. The request should include all necessary supporting documentation.

The timeframe for processing a refund can vary. While some refunds may be processed relatively quickly (within a few weeks), more complex cases or those requiring additional verification may take longer. It’s important to inquire about the estimated processing time when submitting your request.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study