Dealing with insurance can be frustrating. Sometimes, your insurance company might only cover part of your medical bill. An appeal letter for partial insurance payment is your way of requesting them to reconsider. Its purpose is to argue why the denied portion should be covered.

Tired of complicated legal jargon? This article is for you. We understand writing these letters can be tough. That is why we are here. We have gathered templates and samples. You can use these appeal letter for partial insurance payment examples. It will simplify your writing process.

We will provide you with various appeal letter for partial insurance payment formats. Each caters to different scenarios. You can easily adapt these templates. This guide helps you craft a compelling appeal. Get ready to fight for your coverage!

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

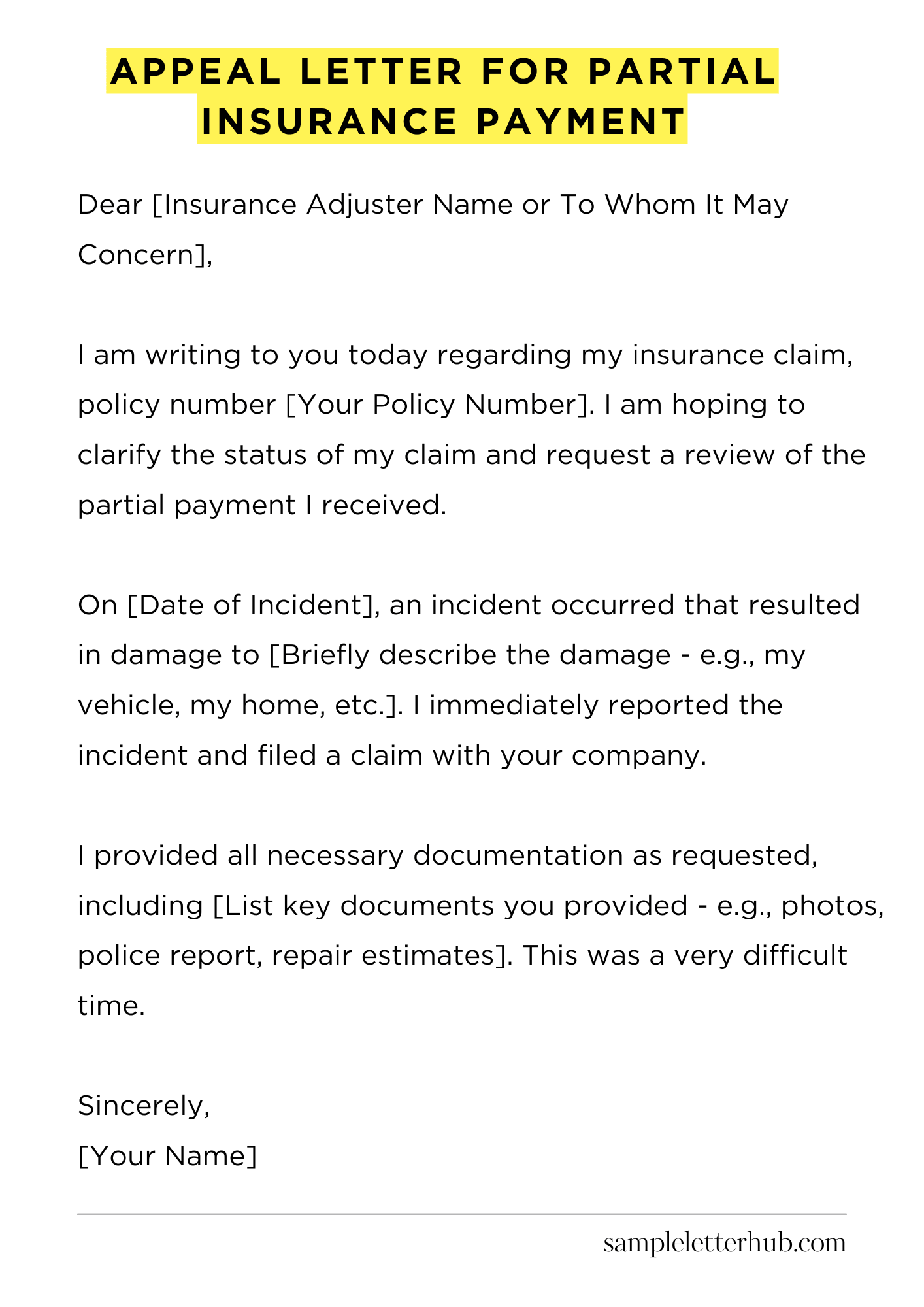

Dear [Insurance Adjuster Name or To Whom It May Concern],

I am writing to you today regarding my insurance claim, policy number [Your Policy Number]. I am hoping to clarify the status of my claim and request a review of the partial payment I received.

On [Date of Incident], an incident occurred that resulted in damage to [Briefly describe the damage – e.g., my vehicle, my home, etc.]. I immediately reported the incident and filed a claim with your company.

I provided all necessary documentation as requested, including [List key documents you provided – e.g., photos, police report, repair estimates]. This was a very difficult time.

I recently received a payment for [Amount of Payment], which I understand is a partial payment for the damages.

I appreciate the initial settlement. However, the total cost of the repairs/damages, as documented in the attached [Mention supporting document – e.g., repair estimate, invoice], is significantly higher, at [Total Cost]. It is a considerable difference, to be sure.

The estimate clearly outlines the scope of the work and the associated costs, and as you can see, the partial payment falls short of covering the full expenses. I have carefully reviewed my policy, and I believe that the covered losses should include the full cost of the repair/replacement. I think the policy covers it very well.

Therefore, I am respectfully appealing for a reconsideration of my claim and a review of the remaining balance. I have attached copies of [Mention any additional supporting documents] for your reference. These will make everything much clearer.

I would greatly appreciate it if you could re-evaluate my claim and consider the evidence provided. I look forward to your prompt response and a resolution to this matter. Please contact me at your earliest convenience if you require any further information.

Thank you for your time and attention to this important matter.

Sincerely,

[Your Name]

How to Write an Appeal Letter for Partial Insurance Payment

Receiving a partial insurance payment can be frustrating, to say the least. It’s a financial hurdle that needs to be addressed with strategic precision.

Don’t simply accept the insurer’s initial decision; you possess the agency to contest it. This guide will walk you through the essential steps to craft a compelling appeal letter, turning the tables in your favor and maximizing your prospects of securing a more equitable settlement.

Prepare to marshal your arguments and advocate effectively for your due compensation.

1. Commence with a Cogent Salutation

Begin your letter with a formal salutation. Address the specific claims adjuster or the relevant department within the insurance company.

If you have the adjuster’s name, use it; otherwise, use a generic title like “Claims Department.” A properly addressed letter indicates you’ve taken the time to be precise, which often reflects well. This small action alone subtly conveys professionalism and seriousness.

2. Explicitly State Your Purpose

The opening paragraph is paramount. Clearly and concisely state the purpose of your letter: to appeal the partial payment. Immediately specify the policy number, claim number, and the date of the denial or partial payment.

Immediately state your disagreement with the insurer’s initial decision. A concise introduction sets the stage for a well-reasoned argument, making it easy for the reader to understand your goals.

3. Detail the Precipitating Circumstances and the Insurer’s Discrepancy

Provide a comprehensive overview of the events leading to the claim. This is a critical section. Outline the facts, including dates, locations, and the nature of the incident.

This is not just a recitation; it is a contextual foundation. Then, directly address the reason given by the insurer for the partial payment. Be specific and systematically counter their justification with facts, documents, and expert opinions.

4. Assemble Compelling Corroborating Documentation

This is where you fortify your assertions with evidence. Attach all supporting documentation to your letter. This may include:

- Police reports.

- Medical records (with HIPAA compliance in mind).

- Photographs and videos of the damage.

- Estimates and invoices.

- Expert witness reports.

Ensure that the documentation is meticulously organized, easy to read, and clearly labeled. Each piece of evidence strengthens your appeal by validating your claims. This provides a compelling tableau of your narrative and validates your position.

5. Decipher the Policy and Explain Your Rationale

Carefully analyze your insurance policy. Scrutinize the language, especially the clauses related to coverage, exclusions, and limitations. Quote directly from the policy to support your case.

Explain how the terms of the policy support your claim for full payment. Show how the insurer has misinterpreted or misapplied a specific clause. This legal analysis demonstrates your understanding of the contract and the insurer’s obligations.

6. Present a Persuasive and Measured Conclusion

Conclude your letter by reiterating your request. State precisely what you are seeking (i.e., the remaining amount of the payment). Reiterate your confidence in your claim and its alignment with the policy’s stipulations.

End with a firm but courteous statement of your willingness to discuss the matter further and your desire for a prompt resolution. Include your contact information (phone number, email, and postal address).

7. Circumspect and Cautious Delivery of the Letter

Mail your appeal letter via certified mail with a return receipt requested. This provides proof of delivery and the date the insurance company received your correspondence.

Retain copies of the letter and all supporting documentation for your records. Consider sending a duplicate copy via email or fax, to expedite the process, but always maintain a physical copy as the authoritative record. After sending the letter, meticulously document all communications and follow-up activities. Be patient, as the appeal process can take time.

FAQs about Appeal Letter for Partial Insurance Payment

What is the primary purpose of an appeal letter for a partial insurance payment?

The main objective of an appeal letter is to formally request a review of an insurance company’s decision regarding a claim. In the context of a partial payment, the appeal seeks to challenge the amount paid, arguing that it does not adequately cover the expenses incurred, as per the terms of the insurance policy.

The letter aims to persuade the insurer to reconsider its initial assessment and provide a more comprehensive payment.

What key information should be included in an appeal letter to increase its effectiveness?

An effective appeal letter should include several critical components. These typically encompass the insured’s personal and policy information, the claim details (date of service, nature of service, and the original claim number), a clear statement of the dissatisfaction with the partial payment.

What are the common reasons insurance companies cite for partial payments, and how can these be addressed in an appeal?

Insurance companies often cite reasons like pre-existing conditions, lack of medical necessity, policy exclusions, or coding errors for partial payments.

When crafting an appeal, it is critical to address the specific reason provided by the insurer. For example, if a pre-existing condition is cited, the insured may need to provide medical records demonstrating the condition was not present prior to the policy’s effective date.

If a lack of medical necessity is the reason, the insured should include documentation from the healthcare provider justifying the treatment.

When the reason is policy exclusions, the insured needs to carefully scrutinize the policy language and demonstrate that the service provided is actually covered under the policy. In case of coding errors, a review by the healthcare provider to correct the codes would be helpful.

What is the typical timeframe for submitting an appeal, and what happens if the deadline is missed?

Insurance companies typically set specific deadlines for submitting appeals, often within a time frame of 60 to 180 days from the date of the payment decision or explanation of benefits (EOB).

The exact timeframe is often detailed in the policy document. Missing the deadline can result in the denial of the appeal. It is therefore crucial to submit the appeal within the stipulated timeframe.

If the deadline is missed, the insured may lose the right to challenge the partial payment, and the initial decision of the insurer is usually considered final. However, some insurance companies might make exceptions on a case-by-case basis; contacting the insurer immediately after missing the deadline could be an option.

What steps should be taken if the initial appeal is denied, and what are the available avenues for further action?

If the initial appeal is denied, the insured may still have options. These can vary depending on the insurance company and the specific policy.

The insured should request a detailed explanation of the denial. Often, the next step involves an internal review by the insurance company, which may involve escalating the case to a higher-level reviewer.

If the internal review upholds the denial, the insured might have the option to pursue an external review, often conducted by an independent organization. As a last resort, the insured might consider legal action, such as filing a lawsuit, depending on the amount in dispute and the specifics of the policy and applicable state laws.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study