You’ve received a settlement from your insurance company. It’s less than you expected. You believe your insurance claim was underpaid. An appeal letter can help. It’s a formal way to dispute the amount. Its purpose is to get the insurer to reconsider.

Don’t worry about where to start. We’re here to help you draft your own. We will provide templates, examples, and samples! We want to make it easy for you. You can use these to craft the perfect appeal letter for underpaid insurance claim.

Our goal? To help you navigate the process. We will help you write a strong letter. This letter will clearly state your case. Get ready to fight for what you deserve. We’ve got the tools. Let’s get started.

[Your Name/Your Company Name]

[Your Address]

[Your City, Postal Code]

[Your Email]

[Your Phone Number]

[Date]

[Insurance Company Name]

[Insurance Company Address]

[Insurance Company City, Postal Code]

Subject: Appeal Regarding Underpaid Insurance Claim – Policy Number [Your Policy Number]

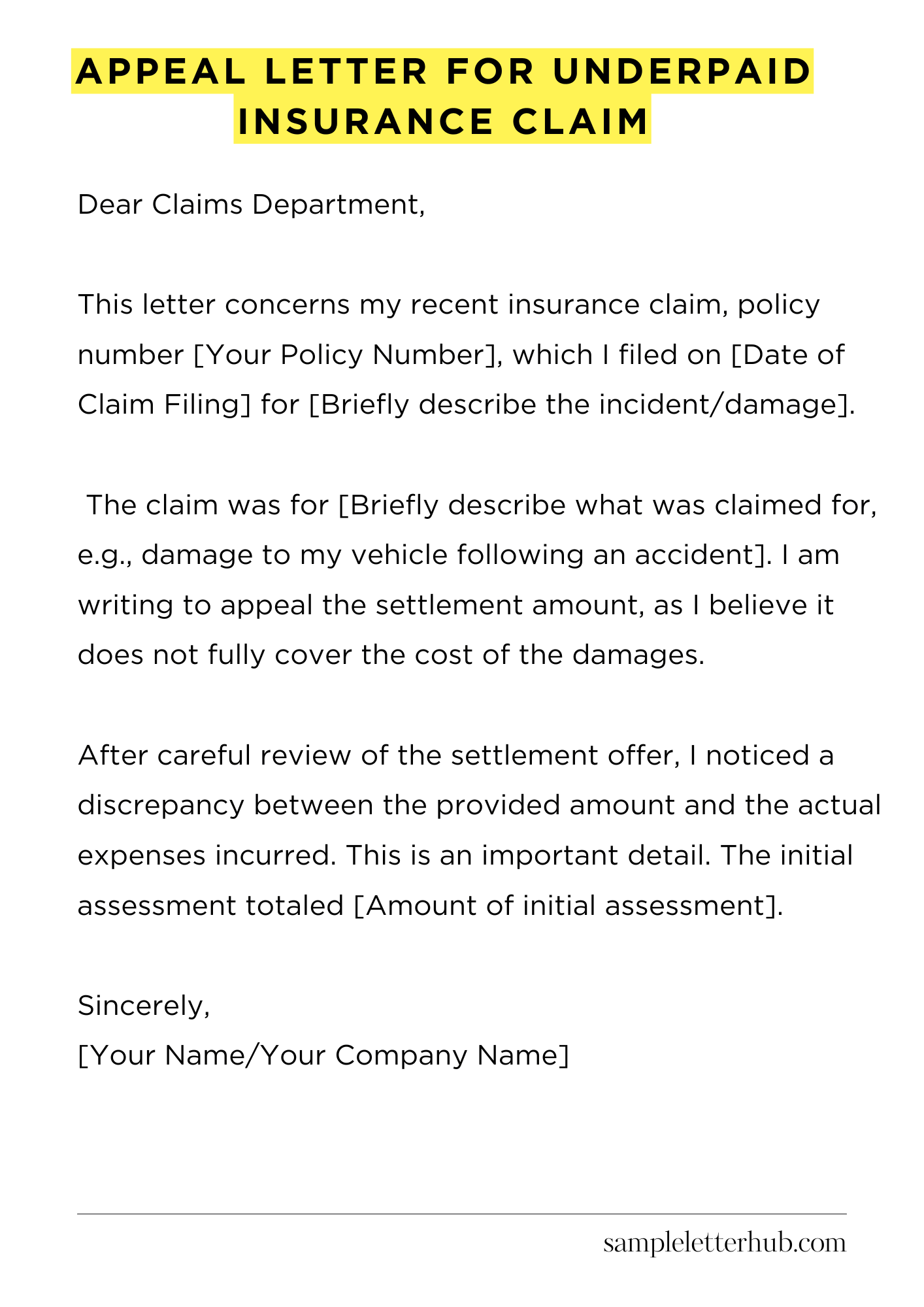

Dear Claims Department,

This letter concerns my recent insurance claim, policy number [Your Policy Number], which I filed on [Date of Claim Filing] for [Briefly describe the incident/damage]. The claim was for [Briefly describe what was claimed for, e.g., damage to my vehicle following an accident]. I am writing to appeal the settlement amount, as I believe it does not fully cover the cost of the damages.

After careful review of the settlement offer, I noticed a discrepancy between the provided amount and the actual expenses incurred. This is an important detail. The initial assessment totaled [Amount of initial assessment].

However, the actual cost of repairs/replacement, as detailed by the attached supporting documents, came to [Actual cost of repairs/replacement]. These documents include [List of documents, e.g., repair estimates, invoices, photographs]. Please take a look at these carefully.

Specifically, the initial assessment undervalued [Specific item or aspect of the claim]. The estimate provided by [Repair shop/relevant professional] clearly outlines the necessary repairs and associated costs, totaling [Specific amount]. You can see the details in the attached documents.

I have also included [Mention any other relevant documents, e.g., police report, expert opinions]. These provide additional support for my claim. These are all crucial to understanding the full extent of the damages.

I kindly request that you reconsider the settlement offer based on the information and documentation provided. It is my sincere hope that the claim can be reassessed fairly and a more appropriate settlement amount can be reached. I believe a just settlement would be [Desired settlement amount, if applicable].

Thank you for your time and attention to this matter. I look forward to your prompt response and a resolution to this issue. Please contact me at your earliest convenience if you require any further information.

Sincerely,

[Your Name/Your Company Name]

How to Write Appeal Letter for Underpaid Insurance Claim

Received an insurance claim settlement that’s less than you anticipated? Don’t resign yourself to a fiscal shortfall just yet. You have recourse: an appeal letter. Crafting a cogent appeal is crucial, acting as your primary advocate in securing a just compensation. Follow these steps to fortify your case and enhance your prospects of a favorable outcome.

1. Scrutinize Your Policy and the Claim Denial

First and foremost, undertake a meticulous review. Analyze your insurance policy meticulously. Become intimately familiar with the fine print, the stipulated coverage, and any exclusions.

Next, meticulously examine the rationale provided by the insurance provider for the underpayment. They will invariably offer a specific justification for the reduction in benefits. Identify any discrepancies, ambiguities, or misinterpretations. This forms the bedrock of your appeal.

2. Gather Supporting Documentation

This is where you amass the evidentiary ammunition. Compile all pertinent documentation. This encompasses medical records (if applicable), repair estimates, photographs documenting damage, bills, invoices, and any other relevant materials. This is an essential step, therefore do not skimp on this.

Ensure each document unequivocally corroborates your claim and substantiates your assertion of underpayment. Organize these meticulously for a seamless presentation.

3. Draft a Compelling Opening

Your opening gambit sets the tone. Begin with a formal and assertive salutation. Clearly state your policy number and the claim number in question. Immediately articulate your grievance: that the received settlement is insufficient and why. Keep it concise. Indicate your intention to appeal the decision.

This is where you grab their attention. Be clear and to the point.

4. Articulate Your Case with Precision

The core of your appeal demands clarity and precision. Construct a persuasive narrative. Detail the circumstances of your claim. Explain the extent of the damage or the medical expenses incurred.

Then, meticulously address the insurance company’s justifications for the underpayment, point by point. Provide counterarguments supported by the documentation you previously compiled. Leverage any external assessments or expert opinions if applicable. The goal is to dismantle their reasoning.

5. Cite Relevant Policy Provisions and Regulations

This demonstrates your diligence and understanding of the contract. Explicitly reference specific clauses from your insurance policy that support your claim. Cite relevant state or federal regulations that apply to your situation.

This underscores the validity of your position. The purpose of this is to build your credibility and strengthen your argument. Knowledge is power.

6. Present a Clear Demand for Remedy

Be explicit in your expectations. State the exact amount of additional compensation you are seeking. Specify how you arrived at this figure, referencing the documentation you presented.

Provide a deadline for the insurance company to respond, typically within 30 days. Maintain a professional and respectful tone throughout, but make your demands unequivocal. Don’t leave room for misinterpretation.

7. Finalize and Submit Your Appeal

Before submitting, meticulously proofread your letter. Verify grammar, spelling, and clarity. Ensure all attachments are included. Submit the appeal via certified mail with return receipt requested.

This provides proof of delivery and ensures accountability. Retain a copy of the letter and all supporting documentation for your records. This is your insurance policy against further complications.

FAQs about Appeal Letter for Underpaid Insurance Claim

What is an appeal letter for an underpaid insurance claim, and why is it necessary?

An appeal letter is a formal written document submitted to your insurance provider to dispute their decision regarding the payout for your insurance claim. It’s necessary because insurance companies sometimes undervalue claims, leading to insufficient compensation for your losses.

The appeal process allows you to provide additional information, challenge their assessment, and potentially receive the full amount you are owed under your policy.

What information should I include in an appeal letter?

A well-crafted appeal letter should contain the following: your policy number, claim number, and the date of the original claim; a clear statement that you are appealing the underpaid claim; a detailed explanation of why you disagree with the insurer’s valuation (referencing specific policy terms, evidence, and supporting documentation).

What is the typical timeframe for filing an appeal, and what happens if I miss the deadline?

The deadline to file an appeal varies depending on your insurance policy and the jurisdiction. However, it’s crucial to review your policy documents or contact your insurance provider to determine the specific timeframe.

Generally, you will have between 30 to 180 days from the date of the claim decision to submit your appeal. If you miss the deadline, your appeal may be rejected, and you might forfeit your right to challenge the underpayment. Therefore, it’s essential to act promptly and meet the stipulated timeframe.

What happens after I submit my appeal letter, and how long does the process take?

After you submit your appeal letter, the insurance company will review your submission, including the supporting documentation you provided. They may request additional information from you or investigate further.

The timeframe for a response from the insurance company also varies, but it is typically a few weeks to several months. You should receive a written response detailing their decision, which may either be an acceptance of your appeal, a denial, or a request for additional information.

If the appeal is accepted, they will provide the revised payment. If your appeal is denied, you may have further options, such as mediation, arbitration, or legal action.

What if my appeal is denied? What are my next steps?

If your initial appeal is denied, you have several potential options. These may include requesting an internal review by the insurance company, pursuing mediation to resolve the dispute with the help of a neutral third party, filing for arbitration (where a neutral arbitrator makes a binding decision), or filing a lawsuit against the insurance company.

The appropriate course of action depends on factors such as the amount of the underpayment, the strength of your case, and the specific terms of your insurance policy. Consider consulting with an attorney specializing in insurance claims to discuss your options and determine the best course of action.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study