Dealing with a denied insurance claim can be frustrating. A dispute letter for denied insurance claim is your formal way of challenging the insurance company’s decision. Its purpose? To convince the insurer to reconsider and pay the claim you believe is rightfully yours. Think of it as your second chance.

We understand the struggle. That’s why we’re here to help! This article is packed with dispute letter samples and templates. We’ll give you examples of dispute letters to make the process easier. Easily craft your own insurance claim dispute letter.

We will provide different denial of claim letter samples. Use these denial of claim letter templates to get your claim approved. Get your claim approved. These samples cover various claim types. This guide simplifies the process.

[Your Name]

[Your Address]

[Your Phone Number]

[Your Email Address]

[Date]

[Insurance Company Name]

[Insurance Company Address]

Subject: Dispute of Denied Insurance Claim – Policy Number [Your Policy Number]

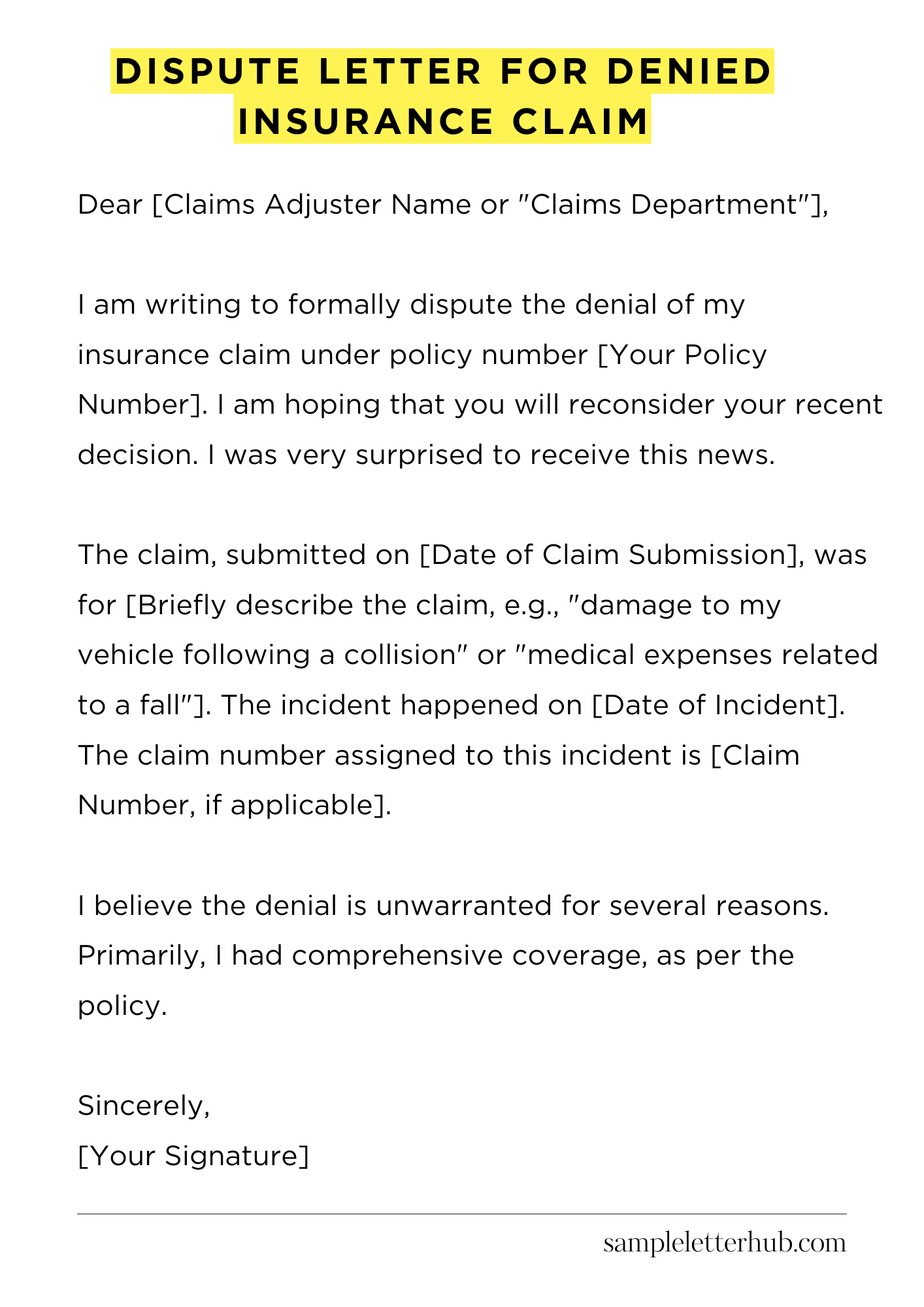

Dear [Claims Adjuster Name or “Claims Department”],

I am writing to formally dispute the denial of my insurance claim under policy number [Your Policy Number]. I am hoping that you will reconsider your recent decision. I was very surprised to receive this news.

The claim, submitted on [Date of Claim Submission], was for [Briefly describe the claim, e.g., “damage to my vehicle following a collision” or “medical expenses related to a fall”]. The incident happened on [Date of Incident]. The claim number assigned to this incident is [Claim Number, if applicable].

I believe the denial is unwarranted for several reasons. Primarily, I had comprehensive coverage, as per the policy. The incident clearly falls under the terms of the policy. I carefully reviewed the policy documents and found no exclusion applicable to my claim.

Furthermore, I have attached copies of [List any supporting documents, e.g., “the police report,” “photographs of the damage,” “medical bills,” “repair estimates”]. These documents provide evidence to support my claim. They clearly show the extent of the damage or the medical necessity.

I am requesting that you thoroughly review my claim again, including all the attached documents. Please give a close eye to all the supporting information. I am confident that upon a full review, you will find my claim to be valid.

I look forward to hearing from you regarding this matter. Kindly let me know the status of this in two weeks. I am eager to get a resolution on this soon.

Sincerely,

[Your Signature]

How to Write Dispute Letter for Denied Insurance Claim

Receiving a denial for an insurance claim can be a frustrating and anxiety-inducing experience. But don’t despair! You have the right to dispute the decision, and a well-crafted dispute letter is your most potent tool.

Let’s delve into the mechanics of composing a persuasive argument that can potentially reverse the insurer’s decision. Follow these stages for the best results.

1. Commence with Thorough Investigation

Before you even pick up your pen (or keyboard), you must become an investigator. First, meticulously review your insurance policy. Scrutinize the fine print, the clauses, and the exclusions. Understand precisely what coverage your policy affords and what it explicitly excludes. This is a crucial first step. Next, analyze the denial letter itself.

Identify the specific reasons cited by the insurer for denying the claim. Was there a procedural misstep, a factual discrepancy, or an interpretation of policy language that you disagree with? Take notes and compile all the supporting documentation.

2. Assemble Your Arsenal: Gather Supporting Documentation

Documentation is the bedrock of your dispute. You need to amass all the supporting evidence to bolster your case. This may include medical records, bills, invoices, receipts, photographs, witness statements, and any other pertinent documents that corroborate your claim. Ensure that all the documents are legible, properly labeled, and organized for easy reference.

Consider creating a concise index or table of contents to further enhance the organization of your submission. This aids in providing comprehensive clarity.

3. Crafting the Compelling Narrative: Structure and Tone

The structure of your letter is paramount. Begin with a clear and concise introduction. State your purpose immediately: you are disputing the denial of your insurance claim. Provide your policy number, claim number, and any other relevant identifiers. The main body of your letter should address each reason for denial cited by the insurer.

For each reason, provide a counter-argument supported by evidence. Be factual, logical, and persuasive. Maintaining a civil and professional tone is essential, even if you are frustrated. This approach increases the likelihood of a successful outcome, which is the ultimate objective.

4. Demystifying the Denial: Addressing the Insurer’s Reasoning

Deconstruct the denial letter. Systematically address each point made by the insurer, providing a rebuttal for each. If the denial cites a specific policy exclusion, carefully explain why that exclusion does not apply to your case. If the denial hinges on a factual dispute, provide evidence that refutes the insurer’s version of events.

If the denial is based on an interpretation of policy language, offer a contrasting interpretation supported by legal precedent or expert opinion. You are essentially painting a picture of your account, which is different from the insurer’s. This is an important step.

5. The Art of Persuasion: Rhetorical Devices and Language

While maintaining a professional tone, strategically use persuasive language. Employ clear, concise sentences. Use active voice over passive voice whenever possible.

Consider using rhetorical devices such as ethos (establishing your credibility), logos (appealing to logic and reason), and pathos (appealing to emotions, but sparingly and appropriately). Avoid jargon, unless you are certain your audience will comprehend it. The clarity and precision of your language will directly influence the success of your letter.

6. The Call to Action and the Finale: Closing Your Letter

Conclude your letter with a clear and definitive call to action. State precisely what you want the insurer to do: reconsider their decision, approve the claim, etc. Set a reasonable deadline for a response.

Clearly state the consequences if they fail to comply (e.g., further escalation, legal action). Thank the recipient for their time and consideration. Be sure to include your name, address, phone number, and email address. Proofread your letter meticulously for any grammatical errors or typos before sending. A well-written letter will leave a lasting impression.

7. Delivery and Follow-up: Finalizing the Process

Send your dispute letter via certified mail with return receipt requested. This provides proof of delivery and ensures that the insurer received your correspondence. Keep a copy of the letter and all supporting documentation for your records.

If you do not receive a response within the specified timeframe, follow up with a phone call or a subsequent letter. Maintain a diligent record of all communications. If the initial dispute is unsuccessful, consider other avenues, such as mediation, arbitration, or legal action.

FAQs about Dispute Letter for Denied Insurance Claim

Understanding the process of disputing a denied insurance claim is crucial for anyone seeking to secure their rightful benefits. Here are the five most frequently asked questions on the topic:

What is a dispute letter for a denied insurance claim, and why is it necessary?

A dispute letter, also known as an appeal letter, is a formal written document submitted to your insurance provider to challenge their decision to deny your claim.

It’s a critical step because it allows you to officially request a review of the denial. It provides an opportunity to present additional evidence, clarify details, and advocate for your coverage. Without a dispute letter, you likely forfeit your right to appeal and potentially lose out on benefits you are entitled to.

What information should I include in a dispute letter?

A comprehensive dispute letter should include your personal information (name, address, policy number), the date of the denial, the specific reason provided for the denial by the insurance company, a clear and concise explanation of why you disagree with the denial, relevant supporting evidence (medical records, bills, photos, etc.)

What is the deadline for submitting a dispute letter?

The deadline for submitting a dispute letter varies depending on your insurance policy and the laws of your state. It’s essential to carefully review your denial letter, as it will usually outline the specific deadline for appeal. Generally, you’ll have 30 to 180 days from the date of the denial to submit your dispute letter.

Missing the deadline means you may lose the right to appeal the decision. If the deadline isn’t mentioned, review your policy or contact your insurance company for clarification.

How should I submit my dispute letter?

It’s crucial to submit your dispute letter in a way that provides proof of receipt. Consider options such as certified mail with return receipt requested, or electronic submission if the insurance company accepts it.

Always retain copies of your letter, all supporting documentation, and proof of submission for your records. This provides a clear timeline and evidence for the insurance company.

What happens after I submit a dispute letter?

After you submit your dispute letter, the insurance company is obligated to review your appeal. The process and timeframe for their response will be outlined in your policy or the denial letter.

They may request additional information, consult with medical professionals, or conduct further investigation. You should receive a written response with their final decision.

If the appeal is denied, you may have further appeal options, such as an internal review or external review by an independent third party, depending on your policy and the specific circumstances.

Related:

Resignation letter due to rude boss

Resignation letter moving to another state

Resignation letter due to illness of family member

Resignation letter due to study